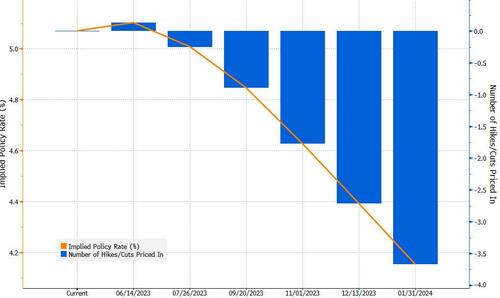

While opinions differed on the margin, the broad consensus is that the Fed just paused its rate hike campaign – pulling a line, literally, from its 2006 FOMC statement when it also was dragged, kicking and screaming, into a Fed pause (before all hell eventually broke loose – after the 10th consecutive rate hike, lifting rates by 25bps to 5.25%. And while the market now sees the Fed as now done and starting to cut as soon as September…

… here is a smattering of Wall Street hot takes on the topic, most of which are largely in agreement.

Jeff Gundlach, Doubleline:

“I suspect the Fed won’t raise rates again”

Bloomberg Economics’ Chief US Economist Anna Wong

“The Fed has marked 5.25% as the terminal rate in this tightening cycle, raising rates by another 25 basis points at the May FOMC meeting — and, more importantly, signaling in the policy statement that this will be the last hike for a while. “Bloomberg Economics expects the Fed to pause at its June meeting, at which point the labor market will be showing clearer signs of softening. We expect the Fed to hold rates at this peak level through 1Q24 as inflation comes down only very gradually.”

Bloomberg Intelligence Chief Rates Strategist Ira Jersey

“The belly of the yield curve is outperforming given the relatively dovish statement from the FOMC, and that may continue beyond today. The removal of the Fed’s ‘firming’ language is telling. It allows the Fed to hike if needed without pre-committing as they basically have during recent meetings. We think they are likely to pause in June, but that’s not a given.”

Bloomberg Economics’ Stuart Paul:

“In his press conference, Powell noted that the balance between labor supply and demand is coming into better balance, with prime participation increasing and job vacancies declining. However, he was clear that the Fed views the labor market as still very tight.”

* * *

“In one of the few answers that he didn’t have well-scripted in the presser, Powell was slow to specify just how tight monetary policy would remain if headline inflation stayed around 3% on a year-over-year basis for a prolonged period of time. At 3% inflation, he acknowledged, the employment and price stability mandates would carry equal weight.”

George Goncalves, head of US macro strategy at MUFG,

“The statement chimes with the Fed’s take back in 2006, when it pushed the funds rate to a peak of 5.25%. They never flat-out come out with ‘we are done’ but this was as close as they could have done so in my book. It’s codified in the statement — like 2006.”

Jan Hatzius, Goldman Sachs chief economist

“As we expected, the FOMC balanced the hint toward a June pause with a clear message that it retains a hawkish bias, noting that it would take into account “the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments” in “determining the extent to which additional policy firming may be appropriate”.

Ellen Zentner, Morgan Stanley

The May statement held little surprise vs our expectation. The Fed delivered a 25bp hike, setting the range of the federal funds rate at 5.00% to 5.25%, and has moved into a conditional pause… We also expected the Fed to memorialize how long rates would remain elevated and it chose not to. That can be interpreted as more dovish than we expected, particularly when compared to Governor Waller’s recent – more hawkish – warning that policy would remain tight for “longer than markets anticipate”.

Ian Lyngen of BMO:

“Powell will strike a dovish tone and stress the heightened uncertainty as the cumulative tightening works its way through the real economy.”

BE’s Anna Wong:

“It’s notable that Powell openly admits he disagrees with Fed staff’s forecasts. Even though Fed governors and presidents don’t always agree with staff forecasts, staff views are often the benchmark that guide members’ forecasts. For the Fed chair to admit he disagrees with staff forecasts is a vote of no-confidence in their reliability.”

Renaissance Macro:

“At this point, the Fed call is a call on the evolution of the economic data. If we are right, the Fed may well be revising up their growth estimates in the June SEP. Events might allow the Fed to skip that meeting, but ultimately, we expect another hike (or two) this year.”

Viraj Patel, Vanda Research

“Given the amount that Powell is talking about credit tightening… SLOOS clearly tightened quite significantly (from already high levels). Now is a case of how persistent that credit tightening is – and how quickly it feeds through to real economy”

Loading…

https://www.zerohedge.com/markets/wall-street-reacts-powells-hawkish-pause

{kind=link}