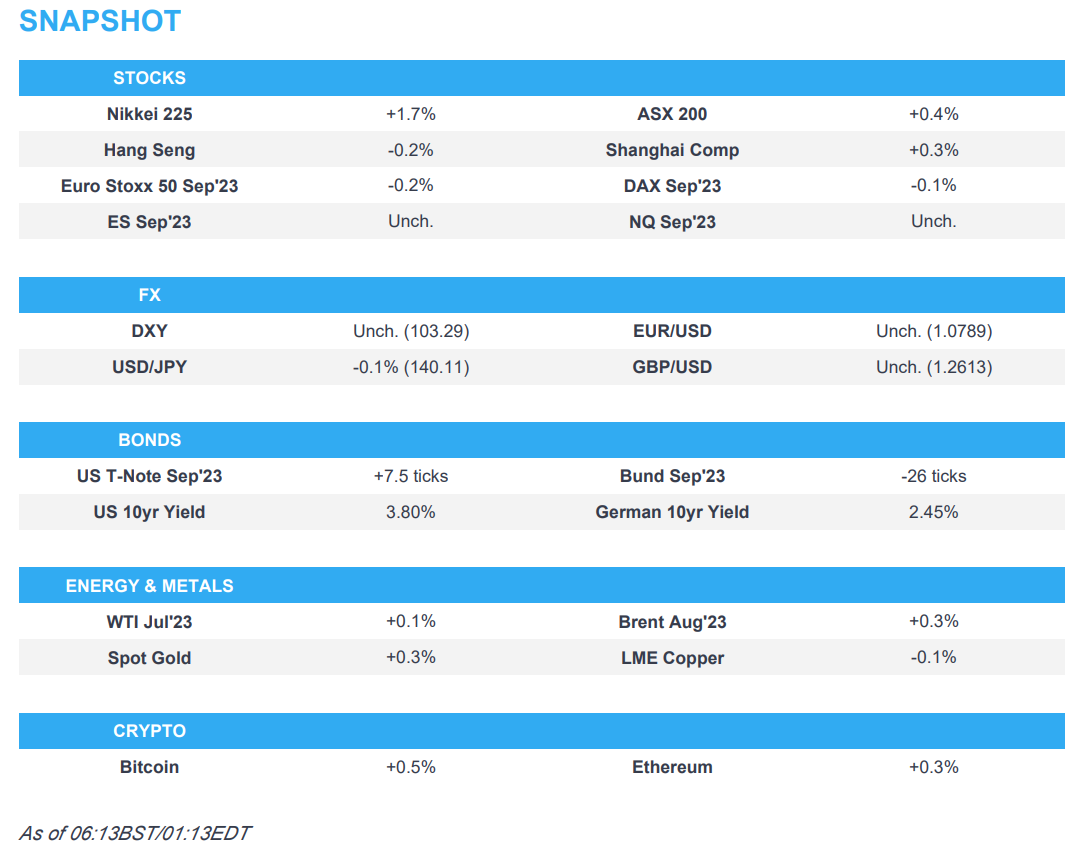

- APAC stocks were somewhat mixed with the region’s bourses mostly tentative despite gains on Wall Street.

- US stocks were firmer after the latest CPI data all but confirmed the likelihood of an unchanged Fed rate.

- European equity futures are indicative of a softer open with the Euro Stoxx 50 -0.1% after the cash market closed up 0.7% yesterday.

- DXY is contained ahead of the FOMC, EUR/USD lingers below 1.08, GBP/USD maintains 1.26 status.

- Looking ahead, highlights include US PPI, EZ Industrial Production, UK GDP Estimate, Sweden CPI, FOMC Policy Announcement & Fed Chair Powell’s Press Conference, Supply from Germany.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were firmer after the latest CPI data including softer-than-expected headline inflation and in-line core figures all but confirmed the likelihood of an unchanged Fed rate, but with upside capped as yields climbed further to post-SVB peaks with WSJ’s Timiraos warning the Fed could increase its Dot Plot.

- SPX +0.69% at 4,369, NDX +0.79% at 14,900, DJIA +0.43% at 34,212, RUT +1.23% at 1,896.

- Click here for a detailed summary.

NOTABLE HEADLINES

- US Treasury Secretary Yellen said the US banking system is still well capitalised and said they will be careful to watch for impacts and market disruption as they build their balance. Yellen also stated they should expect a slow decline in the dollar as the reserve currency and it is important for the dollar to be the world’s reserve currency.

- White House Economic Adviser Ramamurti said macroeconomic trends are reducing US inflation overall.

APAC TRADE

EQUITIES

- APAC stocks were somewhat mixed with the region’s bourses mostly tentative ahead of the FOMC policy announcement.

- ASX 200 was led by strength in the commodity-related sectors after China’s support pledges and PBoC cuts.

- Nikkei 225 extended its advances as automakers and other exporters benefitted from recent currency moves and amid broad consensus for the BoJ to maintain its ultra-easy policy later this week

- Hang Seng and Shanghai Comp. were kept afloat after the PBoC cut rates for its Standing Lending Facility by 10bps and the NDRC issued a notice on lowering costs this year with VAT to be exempted and reduced for small businesses until year-end. China was also said to be weighing broad stimulus with property support and rate cuts, although the gains in Chinese stocks were limited amid ongoing growth concerns and following softer-than-expected loans and financing data.

- US equity futures traded sideways as participants await the incoming Fed policy decision and dot plot forecasts.

- European equity futures are indicative of a softer open with the Euro Stoxx 50 -0.1% after the cash market closed up 0.7% yesterday.

FX

- DXY was rangebound heading into the FOMC policy decision with the central bank widely expected to skip raising rates.

- EUR/USD traded steadily and looked to retest 1.0800 after yesterday’s brief incursion above the level.

- GBP/USD held on to the 1.2600 status and took a breather from recent advances which were facilitated by firm jobs and earnings data, while participants will also get to digest the latest UK GDP estimates and Industrial Production figures.

- USD/JPY eased back from its recent peak but with the reversal contained by support at the 140.00 level.

- Antipodeans were rangebound with early gains in NZD owing to cross-related flows and after New Zealand Current Account data printed at a narrower than expected deficit.

- PBoC set USD/CNY mid-point at 7.1566 vs exp. 7.1550 (prev. 7.1498)

FIXED INCOME

- 10yr UST futures pared some of the losses from the recent bear-flattening after yields rose to post-SVB peaks.

- Bund futures moved off their lows but remained subdued ahead of this week’s trifecta of major central bank meetings.

- 10yr JGB futures were lacklustre in the absence of additional BoJ purchases but with losses cushioned by a floor at the 148.00 level.

COMMODITIES

- Crude futures were rangebound and took a breather after yesterday’s recovery which was spurred by Beijing’s efforts to bolster the economy, while further upside was restricted by private sector inventory data which showed mild builds across all products.

- US Energy Inventory Data (bbls): Crude +1.0mln (exp. -0.5mln), Gasoline +2.1mln (exp. +0.3mln), Distillate +1.4mln (exp. +1.2mln), Cushing +1.5mln.

- US DoE said it is continuing to seek opportunities for more purchases and is to buy roughly 12mln bbls of oil in 2023 to boost reserves with the total including barrels already announced for August and September, according to Bloomberg.

- Spot gold was contained alongside an uneventful dollar.

- Copper futures plateaued overnight but held on to the prior day’s gains which were spurred by the PBoC’s short-term funding rate cuts and China’s recent policy support pledges.

CRYPTO

- Bitcoin was indecisive in which prices oscillated in a tight range around the USD 26,000 level.

- Binance and SEC are reportedly not far apart on a deal to avoid a full asset freeze, according to Bloomberg.

- Binance CEO Zhao denies rumours of selling Bitcoin to bolster BNB, according to Cointelegraph.

NOTABLE ASIA-PAC HEADLINES

- Chinese Foreign Minister Qin Gang held a call with US Secretary of State Blinken and said the US should stop interfering with China’s internal affairs and should respect China’s concerns such as the Taiwan issue, while he added the US should stop hurting China under the excuse of competition and hopes the US will meet China halfway, effectively manage differences and promote communication and cooperation, according to state media.

- Japanese PM Kishida is reportedly considering dissolving the Lower House of Parliament on the same day if the opposition submits a no-confidence vote on Friday, according to Fuji TV.

DATA RECAP

- New Zealand Current Account (Q1) -5.2B vs. Exp. -6.8B (Prev. -9.5B)

- New Zealand Current Account/GDP (Q1) -8.5% vs. Exp. -9.0% (Prev. -8.9%)

GEOPOLITICS

- Russian President Putin said they are considering withdrawing from the grain deal.

- Russian official said nuclear safety at the Zaporizhzhia plant will be fully secured, according to TASS.

- NATO Secretary General Stoltenberg said Ukraine is making progress in its counter-offensive.

- US CIA warned the Ukrainian government not to attack the Nord Stream gas pipelines last summer after it obtained detailed information about a Ukrainian plot to destroy a main energy connection between Russia and Europe, according to WSJ citing sources.

- Russia urged for a transparent investigation into the Nord Stream blasts after reports that the US warned Ukraine not to attack Nord Stream, according to Reuters.

- White House said US President Biden met with the NATO chief and they underscored their shared desire to welcome Sweden to the alliance ASAP, while they also discussed the need for allies to build on the 2014 Wales summit defence investment pledge.

- Israeli PM Netanyahu said the Biden administration has held indirect talks with Iran on a “mini agreement” or “an understanding” related to Iran’s nuclear program, according to Axios citing sources. However, it was separately reported that the US State Department said it is completely false that there is an interim nuclear deal with Iran.

EU/UK

NOTABLE HEADLINES

- French Finance Minister Le Maire vowed to put France’s finances back on track with spending cuts, according to FT.

- European Commission President von der Leyen said the EU is to invest USD 10bln in LatAm and the Caribbean.

- EU is looking to pass a renewable energy deal on Wednesday which would include an exemption for certain ammonia plants, according to Reuters sources.

- Downing Street has ordered banks to protect struggling homeowners from increasing mortgage costs as markets speculate over the possibility of the Bank Rate rising to as high as 6%, according to The Telegraph.

Loading…

https://www.zerohedge.com/markets/tentative-trade-ahead-fomc-policy-announcement-newsquawk-europe-market-open

{kind=link}