Authored by Simon White, Bloomberg macro strategist,

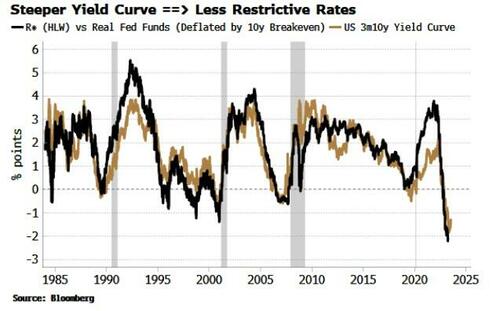

A steepening US yield curve would mean less restrictive rates.

It’s early days, but there are tentative signs of a trend change in the yield curve.

The 2s10s curve has steepened ~25 bps in the last week. Other parts of the curve, such as 3m10y and 5s30s have also steepened.

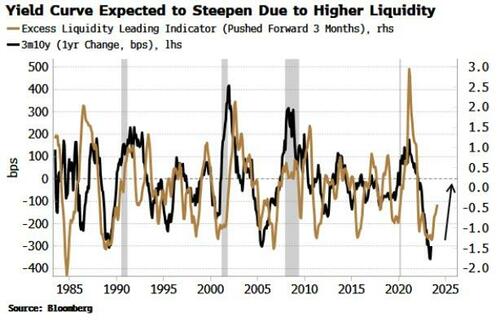

There are indications this trend will continue. Excess liquidity has been rising and this points to further steepening.

More buoyant liquidity conditions likely mean a preference for riskier assets at the margin, i.e. stocks over bonds, as well as a preference for lower-duration bonds as the velocity of money rises.

The Fed’s rate-hike campaign has left real rates very restrictive. A steepening yield curve would alleviate some of this restriction, further aiding risk assets.

Higher nominal rate expectations have driven longer-term yields which have in turn led the yield curve steeper. Term premium, in simplified terms the market’s expectation of higher inflation, has been steady. However, that could change later in the year if we see a re-acceleration in inflation.

Term premium would then likely rise, causing the curve to steepen in a way that would not be indicative of a positive environment for risk assets.

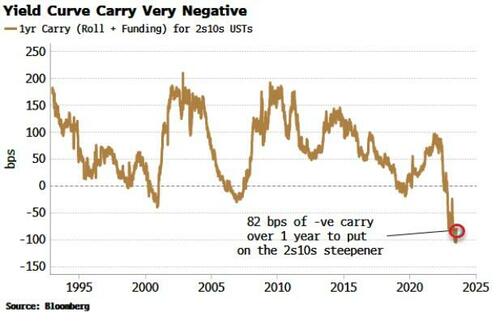

Nonetheless, in the shorter term, the yield curve faces some resistance from carry.

If we look at the total carry cost (roll + funding) for an investor putting on a 2s10s steepener in USTs one year forward, there is over 80 bps of negative carry on that position – the biggest it’s been for several decades (consistent with the extreme depth of the curve’s inversion).

Loading…

https://www.zerohedge.com/markets/steeper-us-yield-curve-promises-less-restrictive-rates

{kind=link}