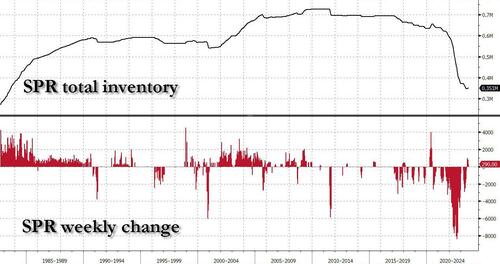

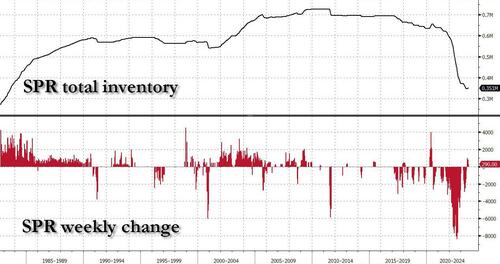

After languishing a multi-year lows until the end of June in the low/mid-70s range after Biden drained over 270 million barrels from the SPR to a near record low in hopes of pushing the price of gasoline lower and achieving short-term political goals…

… oil has since surged by more than $20, or 32% since the low of $71.57 on June 28, its fastest ascent since the start of 2022, a rally that was sparked by Saudi Arabia’s decision to voluntarily cut an additional 1 million bpd of production in addition to the reductions agreed by the OPEC+ group…

… thereby intentionally creating a production deficit of over 3 million barrels per day.

As such the price is likely to keep rising well into the 100s, as we first predicted two weeks ago, and as Chevron CEO Mike Wirth said today on BBG TV.

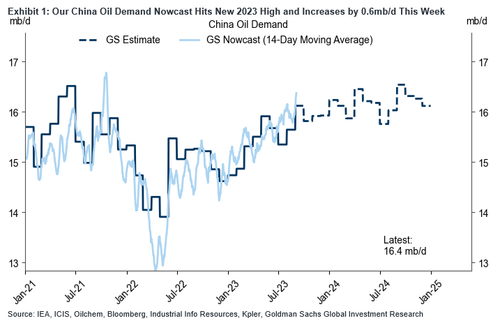

Meanwhile, even as China remains the biggest bullish upside case because it is only a matter of time before all the piecemeal stimuli injections lead to economic overheating and much higher demand for commodities, oil demand in China is already at the highest level in 2023.

Yes, even though China’s economy remains (for now) in the doldrums, Beijing keeps buying up every barrel it can find just as it keeps on stockpiling every other type of commodity…

China currently holds 96% of global copper inventories, 75% of global aluminum, 70% of corn, 54% of wheat, 30% of soybeans and 22% of crude oil: JPM

— zerohedge (@zerohedge) January 24, 2023

… almost as if it is preparing for war.

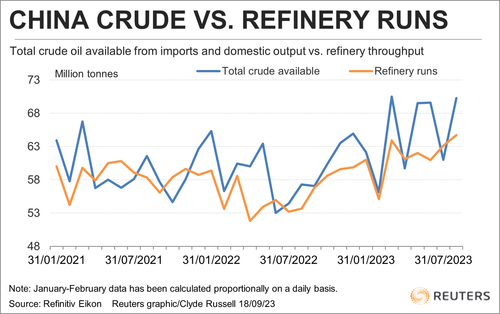

Indeed, China’s endgame intentions aside, Reuters reports while that the country’s record crude oil processing and robust imports in August have painted a bullish picture of demand in the world’s largest importer, “what is largely ignored, but shouldn’t be, is the vast quantities of oil flowing into inventories.”

Citing official data, Reuters calculated that China added about 1.32 million barrels per day to either commercial or strategic crude stockpiles in August, with Platts calculating that China’s crude inventory – comprising commercial and SPR – hit a record high 1.142 billion barrels in July. This comes at a time when similar US crude inventories have dropped to just over 770 million barrels, and are rapidly depleting.

China’s oil buildup to record oil inventory levels reversed a rare draw in July, when refiners processed about 510,000 bpd more than was available to them from imports and domestic production.

As we noted last month, July was the first month in 13 that China turned to stockpiles, and came at a time when imports dropped as crude prices rose during the period when July-arriving cargoes would have been arranged. This was reversed in August as strong crude imports and steady domestic output outweighed the record refinery processing rates.

While China doesn’t disclose the volumes of crude flowing into or out of strategic and commercial stockpiles, one can make an estimate by deducting the amount of crude processed from the total of crude available from imports and domestic output.

According to the latest data released by China’s National Bureau of Statistics, the country’s refiners processed 64.69 million metric tons in July, equivalent to 15.23 million bpd. This was up 19.6% from the same month in 2022 and also stronger than July’s 14.87 million bpd.

At the same time, crude imports were 12.43 million bpd in August – the third-highest daily rate on record and up 20.9% from July and 30.9% from August last year – while domestic oil output was 4.11 million bpd in August, which when put together with imports means a total of 16.55 million bpd was available to refiners.

Subtracting processing of 15.23 million bpd leaves a surplus of 1.32 million bpd that flowed into storage tanks.

Putting this together means that for the first eight months of the year China added about 810,000 bpd to inventories, or a total of about 197 million barrels. This means that in theory China could lower imports by about 1.61 million bpd over the final four months of 2023 and still have stockpiles at exactly the same level as they were at the end of 2022, not that China will do that of course, as it appears hell bent on storing every ounce of oil it can get its hands on (the question, again, is why, but we’ll leave that to much smarter folks than us to answer).

In practical terms, China’s stockpiling spree means that China’s refiners could maintain strong processing rates in order to meet domestic demand and lift exports of refined fuels in order to capture high margins, especially for diesel. They could do this while lowering imports, which in turn may put some downward pressure on crude oil prices, which hit a 10-month high on Sept. 15.

The rally since late June was largely sparked by Saudi Arabia’s decision to voluntarily cut an additional 1 million bpd of production in addition to the reductions agreed by the OPEC+ group, of which the Saudis are the leading exporter.

The question now, according to Reuters, is how will China’s refiners respond to the higher crude oil prices? History suggests that they tend to pare imports if they take the view that prices have risen too fast or too high. Conversely they tend to import more and fill storage tanks when prices are low. And so far, China has given zero indication it will slow down its pace of imports.

Still, given that prices started to rally strongly from July onwards, if China’s refiners do trim imports, it will likely only show up from September, or more likely October, given the lag between when cargoes are arranged and physically delivered. That said, China is unlikely to reduce imports in the fourth quarter, especially since its refiners can continue to access discounted oil from Iran, Russia and Venezuela.

But there is a risk that they do turn to stockpiles and it’s a risk that the market seems to be largely discounting.

That’s not a view that is widely shared by the industry, and as crude futures leap higher, traders and analysts are increasingly talking about when, not if, prices return to $100 a barrel.

Among the bullish signs that scream triple-digit oil, we see that across the world, premiums for physical barrels are surging, and supplies from the Middle East, Azerbaijan and even Russia are commanding premiums as refiners clamber to make enough diesel ahead of a seasonal ramp up in demand.

Bullish analysts argue that even with crude now in the mid-$90s, many funds remain underinvested in oil, creating the potential for higher prices yet to come. Speaking on BBG TV, Chevron CEO Mike Wirth sees oil reaching $100 a barrel.

“Fundamentals are very, very strong right now,” Amrita Sen, head of research at consultant Energy Aspects, said on Bloomberg Television. “At this point it’s a short-term thing. I’m not saying it’s going to average above $100, but could it go to $100 for a bit? Absolutely yes.”

The strength, Bloomberg notes, is being led by the physical markets. One of the clearest examples is Azerbaijan’s flagship Azeri Light crude, which was trading close to $100 a barrel Friday as strong profits for turning crude into diesel mean processors are paying bumper premiums for grades that produce a lot of the fuel (something we discussed over a month ago in “US Diesel Prices Surge Anticipating A Soft Landing”).

Those same margins also see once-maligned Russian barrels trading above their benchmark in Asia again, traders said. They were at a discount for much of the time after the country’s invasion of Ukraine.

The strength shows up in the shape of the oil futures curve, too. On Monday, the nearest Brent futures contract was at a premium of more than $1 a barrel to the next month. The structure, known as backwardation and indicating scarce supply, was the biggest since November, excluding expiry days. It’s against that backdrop that even some of the market’s most bearish analysts are starting to concede that $100 looks more likely, particularly given longstanding political risks in producers such as Libya and Nigeria.

Geopolitics, alongside technical trading, “could push oil over $100 for a short while,” Citigroup analysts, including oil permabea rEd Morse, wrote Monday, admitting he had been dead wrong for 2023 with his doomsday oil price predictions. “However, we continue to see progressive loosening on the horizon” he added, because of course he will be right… eventually.

Part of that decline, Citi argues, will be driven by a growth in supply from outside the OPEC+ alliance. It cites countries — including the US, Guyana and Brazil — that can all add barrels to the market in coming months and derail the current tightness.

For now, though, revenue in producing nations is surging. On Friday, Murban oil from the United Arab Emirates was trading at the strongest level since February and rose further on Monday. Barrels from Qatar to West Africa also are soaring, and Saudi Arabia’s flagship grade is near $100.

Those spikes are shifting the focus to demand and the impact on consuming nations. The Reserve Bank of India said Monday that crude oil above $90 a barrel poses a new risk to global financial stability, although one wonders where that math comes from: after all, oil was trading well into the triple digits more than a decade ago when inflation was far, far below where it is now. In fact, in inflation-adjusted terms, one can argue that oil has rarely been this cheap!

While Brent is yet to hit triple digits this year, refined fuels such as gasoline and diesel have been trading above that level for months.

“We are highly likely to see Dated Brent moving above $100 a barrel,” said Bjarne Schieldrop chief commodities analyst at SEB AB. “But oil product demand is likely to hurt more if Brent crude rises to $110-$120 a barrel, and such a price level looks excessive.” Perhaps, but the market will be certain to test just how high it can take oil now that momentum is very clearly in just one direction.

Loading…

https://www.zerohedge.com/markets/oil-surges-95-china-crude-stockpiles-hits-record-114-billion-barrels

{kind=link}