The second quarter – and first half – of 2023 is coming to a close on an upbeat note, as US equity futures are higher, led by megacap tech, and especially Apple, which is set to open with a market cap over $3 trillion following a bizarre initiation report from Citi yesterday late, which set a $240 price target on the world’s biggest company, just in time to catch its all time high. As of 7:45am ET, S&P futures were 0.4% higher, set to close out a third straight quarterly gain…

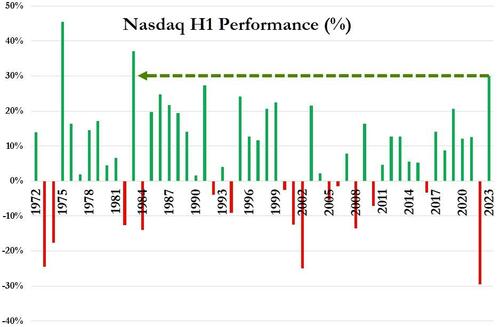

… while Nasdaq futures rose 0.5%, indicating the index is set to extend its 37% surge since the start of the year, its best start to the year since 1982.

Treasuries extended a selloff, with yields rising 4-6 bps across the curve as two-year yields rose about five basis points to 4.92%, adding to Thursday’s 16-point jump. The 10-year yield increased three points to its highest level since mid-March. Swap markets now indicate a nearly 50% chance of a second US hike by year-end sparked by robust US economic growth and jobs data that fueled bets on more interest rate hikes. The USD is higher, and commodities are mixed with the energy complex higher and base metals lower. Today, focus will be on the latest PCE report where consensus expects core PCE to print 4.7% vs. 4.7% prior and headline PCE to drop to 3.8% vs. 4.4% prior. In addition, keep an eye on Personal Income/ Spending, MNI Chicago PMI and the revision of UMich. data. Also, the supreme Court will decide on Biden’s student loan forgiveness today.

In premarket trading, it was a less positive picture for sportswear giant Nike, whose shares fell 3.7% after the retailer’s outlook for the full year failed to impress. While sales beat forecasts, however, and analysts highlighted Nike’s better-than-anticipated performance in China as a bright spot. The results also showed Nike is still working to sell off its high stockpiles of merchandise that have eroded profitability. “Nike is a solid brand,” said Neil Saunders, an analyst at GlobalData Retail. But “it isn’t on the front foot either, and has to accept that the year ahead will be one of resetting, retrenching, and reformulating the way it does business.” Here are some other notable premarket movers:

- Apple shares rise 0.8% in premarket trading Friday, with the iPhone maker’s market value set to exceed the historic $3 trillion threshold.

- Aurinia Pharmaceuticals shares jump as much as 19% in US premarket trading after the drug developer said that it is exploring options, including a sale. Analysts say the announcement is positive for the shares and could see the company being an attractive target for a bigger pharma firm in the rheumatology space, touting a possible takeout price in the high teens.

- XPeng shares jump over 7% in US premarket trading after the Chinese company unveiled its new G6 electric SUV. Analysts say the product has a competitive price and could stock sales.

- Smart Global shares rose 5.2% in post-market trading after the company forecast adjusted earnings per share for the fourth quarter that exceeded the average analyst estimate at the midpoint.

Thursday’s readings on US jobless claims and the gross domestic product showed the world’s biggest economy was in better shape than many had envisioned at the start of 2023. After the data came out, the US yield-curve inversion intensified — with longer-dated yields rising less than shorter-maturity ones. That means the economy may look stronger now, but investors expect the Fed’s rate increases to curb future growth, which could boost the risk of a recession down the road.

Bets on further Fed tightening will be will be tested by US price measures due Friday, including figures on personal income and spending as well as the PCE deflator, the Federal Reserve’s preferred gauge of underlying inflation pressures. The numbers are expected to show some softening while still indicating inflation remains sticky.

“Markets are still really caught up in the ‘strong data’ narrative,” said James Rossiter, head of global macro strategy at TD Securities. “But ultimately the Fed’s going to be focused on where inflation is right now. It’s going to be a more difficult decision for them in July, especially given how much tightening they’ve already put in the system that still has to play out.”

The Stoxx Europe 600 index climbed more than 1% led by energy, real estate and banks, with all sectors rising barring tech. Euro Stoxx 50 rises 0.6%. FTSE MIB outperforms peers, adding 0.9%, FTSE 100 lags, adding 0.6%. Among individual movers, Engie SA rose after the French utility raised its full-year earnings forecast. ASML Holding NV dropped after the Dutch chipmaker was slapped with more restrictions on exports to China. The European benchmark is on track to end the quarter flat after failing to build on its 7.8% first-quarter gain amid outflows from European stocks totaling $27 billion this year. A gauge of global equities, meanwhile, headed for a quarterly rise of 4.5%, defying rising interest rates and the risk of recessions in major economies. Here are today’s most notable movers:

- Kion shares rise as much as 7.6%, the most since November, with Warburg expecting the German warehouse equipment firm to present solid second-quarter figures on 27 July

- LEG Immobilien jumped 7.5% after the German real estate company boosted its guidance for adjusted funds from operations and EBITDA margin for the full year, boosting the whole real estate sector

- Steico rises as much as 11% after Morgan Stanley raised its recommendation to overweight, saying the manufacturer of insulation materials is close to the bottom of the downgrade cycle

- Societe Generale rises as much as 2.3% to a one-month high after Deutsche Bank raised its recommendation to buy from hold, noting tailwinds for 2024 such as a recovery in NII

- Engie rises as much as 2.7% after the French utility raised its FY earnings forecast. Morgan Stanley attributes the guide upgrade stems to the company’s global energy management and sales

- Drax shares climb as much as 3.9% after Credit Suisse raised its recommendation on the British utility to outperform saying the valuation looks attractive on most cashflow-based metrics

- Nordex rises as much as 4.5% after Deutsche Bank initiated coverage of the German wind turbine maker with buy, saying it’s well-positioned in most key regions with impressive recent share gain

- ASML falls as much as 3.8%, its biggest intraday decline since April, after a Reuters report said the US plans to force the company to ship fewer of its deep ultraviolet lithography machines to China

- Bawag shares fell the most in more than three months, tumbling as much as 14% in Vienna, after activist investor Petrus Advisers Ltd. published a report that identified potential red flags

- Aperam slides as much as 7.1% after the steelmaker was downgraded by two brokerage firms. Degroof Petercam cuts the stock to hold, citing a lack of short-term visibility on earnings recovery

- Fevertree shares drop as much as 7.4%, the most intraday since April 27, after Bank of America cut its recommendation on the high-end tonic maker to underperform, citing an “unjustified” valuation

Earlier in the session, Asian stocks traded with cautious gains amid the higher yield environment and as participants digested a slew of data releases at quarter-end including the latest Chinese official PMIs.

- Hang Seng and Shanghai Comp were initially choppy but ultimately gained after the latest Chinese PMI data in which headline Manufacturing PMI matched estimates and Non-Manufacturing PMI was slightly softer-than-expected although remained at a firm expansion.

- ASX 200 lacked direction as gains in the commodity-related sectors and utilities offset losses in real estate and tech.

- Nikkei 225 was subdued after mixed data releases including disappointing Industrial Production and softer-than-expected Tokyo CPI although the losses were cushioned as USD/JPY briefly climbed above 145.00.

In FX, the Bloomberg Dollar Spot Index remains little changed; NOK/USD leads G-10 gains climbing 0.5%, while EURUSD slumps 0.2% after data showed euro-area core inflation re-accelerating. The yen briefly weakened past 145 for the first time since November, putting markets on watch for possible Japanese intervention. It since retraced to around 144.70 after Finance Minister Shunichi Suzuki told reporters the government would respond appropriately to any excessive moves in the currency market. The offshore yuan remained in the spotlight after the recent slide to its lowest level in seven months. It appreciated Friday, for the first time in three days, after the People’s Bank of China again set the daily reference rate for currency at a level stronger than the average estimate in a Bloomberg survey. The currency is down almost 5% against the dollar this year, prompting extra scrutiny from Chinese regulators, according to people familiar with the matter. Purchasing managers’ index data from China on Friday underscored concern that the economy is losing steam, bolstering calls for more policy support.

In rates, treasuries extended a weekly slide gilts fall sharply following a bundle of UK economic data. Treasury losses continued to be led by front-end and belly of the curve, deepening inversion of 2s10s, 5s30s spreads. Yields on the two- year climbing six basis points to 4.92% and yields on the 10- year rising 4 basis points to 3.88%; euro bonds see broad-based selling. 2s10s, 5s30s spreads flatter by 1.3bp and 2bp on the day; 10-year yields around 3.87%, cheaper by 3bp vs Thursday close. Yields except 30-year are at highest levels since March as expectations have mounted for two more Fed rate increases this year, and the Bloomberg Treasury Index is headed for a second straight monthly loss. Month-end index rebalancing at 4pm is estimated to extend its duration by 0.07 year. US session includes May personal income and spending report that embeds PCE deflators.

Yields on European bonds retreated from session highs and the euro pared a decline after data showed inflation in the common-currency area slowed more than economists’ expectations in June. Core prices re-accelerated, though, in a setback for the European Central Bank that may reinforce its determination to raise interest rates next month.

“An extra interest rate hike at the next monetary policy meeting is nearly a done deal,” said Daniele Antonucci, chief economist and macro strategist at Quintet Private Bank. “Further out, the picture is less clear. How far the ECB will have to go remains an open question and depends on how much it’s willing to sacrifice in terms of job losses.”

In commodities, WTI drifts 1% higher to trade near $70.54. Brent crude oil is on track for the worst run of quarterly losses in three decades as persistent concerns over the demand outlook and robust supplies weigh on prices. Spot gold falls roughly $5 to trade near $1,903/oz.

Bitcoin is on a firmer footing intraday but remains under the USD 31k level. RBNZ is to ramp up monitoring of stablecoins and crypto assets but noted that regulation of crypto assets is not currently required.

Looking at today’s data, releases include the Euro Area flash CPI reading for June. In Germany, we’ll also get retail sales for May and unemployment for June. And in the US, there’s the PCE reading for May, and personal income and personal spending data.

Market Snapshot

- S&P 500 futures up 0.1% to 4,442.00

- MXAP down 0.2% to 162.88

- MXAPJ little changed at 512.81

- Nikkei down 0.1% to 33,189.04

- Topix down 0.3% to 2,288.60

- Hang Seng Index little changed at 18,916.43

- Shanghai Composite up 0.6% to 3,202.06

- Sensex up 1.0% to 64,562.15

- Australia S&P/ASX 200 up 0.1% to 7,203.30

- Kospi up 0.6% to 2,564.28

- STOXX Europe 600 up 0.7% to 459.63

- German 10Y yield little changed at 2.45%

- Euro down 0.2% to $1.0839

- Brent Futures up 0.9% to $75.02/bbl

- Gold spot down 0.4% to $1,900.84

- U.S. Dollar Index up 0.18% to 103.53

Top Overnight News from Bloomberg

- China’s June NBS PMIs better than feared, with manufacturing ticking up to 49 (vs. 48.8 in May and inline w/the Street) while services cool to 53.2 (down from 54.5 in May and a tiny bit below the Street’s 53.5 forecast). RTRS

- U.S. counterintelligence officials are amping up warnings to American executives about fresh dangers to doing business in China under an amended Chinese law to combat espionage. WSJ

- Japan’s Tokyo CPI for June undershoots the Street, coming in at +3.1% headline (vs. the Street’s +3.4% and down from +3.2% in May) and +3.8% core (vs. the Street’s +4% and down from +3.9% in May. BBG

- ECB’s hawkishness in part a function of events in the UK where inflation continues to surprise to the upside (ECB officials don’t want to take their foot off the tightening gas until they are absolutely certain core inflation is on a sustainable downward trajectory). FT

- Eurozone CPI for June undershoots the Street, with headline coming in at +5.5% (vs. the Street +5.6% and down from +6.1% in May) and core +5.4% (vs. the Street +5.5% and up from +5.3% in May). BBG

- “Shaky” flows into Pimco are prompting Allianz to push deeper into alternative asset classes such as real estate, where manager’s fees tend to be higher and client assets are stickier. While the bond manager attracted €14 billion in the first quarter after a €75 billion streak of outflows, investors are still skittish, Allianz CEO Oliver Baete said. BBG

- PCE: Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.32% month-over-month in May, corresponding to a 4.64% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.13% in May, corresponding to a 3.87% increase from a year earlier. We expect that personal income increased by 0.5% and personal spending increased by 0.2% in May. GIR

- NKE delivered a solid F4Q23 revenue result, with stronger DTC growth and momentum in Greater China driving the outperformance. However, we note that this was offset by weaker than expected F4Q margins and a below-consensus F1Q guide. We step away from the quarter with our constructive view intact. While near-term growth and margins are more challenged than our expectations on wholesale shipment timing / liquidation sales / transitory cost headwinds / SG&A investments, we believe this quarter continued to deliver several key proofpoints of the bull case. GIR

- META is planning to allow people in the EU download apps through Facebook ads, a move that will eventually put it in direct competition w/the app stores from Google and Apple. The Verge

- Nasdaq 100 GREEN in July 15 consecutive years with an avg return of +4.64%…

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly traded with cautious gains amid the higher yield environment and as participants digested a slew of data releases at quarter-end including the latest Chinese official PMIs. ASX 200 lacked direction as gains in the commodity-related sectors and utilities offset losses in real estate and tech. Nikkei 225 was subdued after mixed data releases including disappointing Industrial Production and softer-than-expected Tokyo CPI although the losses were cushioned as USD/JPY briefly climbed above 145.00. Hang Seng and Shanghai Comp were initially choppy but ultimately gained after the latest Chinese PMI data in which headline Manufacturing PMI matched estimates and Non-Manufacturing PMI was slightly softer-than-expected although remained at a firm expansion.

Top Asian News

- China may announce more property market support measures although measures might be incremental, while China is expected to revise certain home purchase restrictions and has room to lower the down payment ratio, according to China Securities Journal.

- PBoC set USD/CNY mid-point at 7.2258 vs exp. 7.2525 (prev. 7.2208).

- PBoC surveyed some foreign banks about USD deposit rates, according to Reuters sources.

- Japan Chief Cabinet Secretary Matsuno said sharp, one-sided currency moves are seen recently, and they are closely watching FX moves with a high sense of urgency. Matsuno said they are to take appropriate steps on excess FX moves, according to Reuters.

- Japan MOF says FX intervention amounted to JPY 0.00 in the period from May 30th to June 28th, according to Reuters.

European bourses trade on the front-foot with the Stoxx 600 on track to close the week out with gains, with little action seen on the EZ Flash CPI metrics. US equity futures are around flat/tilting higher ahead of today’s key PCE data for May, before traders head out for the long Independence Day holiday weekend. Equity sectors in Europe are higher across the board with the exception of technology which is being weighed on by ASML which is also acting as a drag on the AEX following news that the Dutch Foreign Ministry has issued new computer chip equipment export rules whereby an export license will be required for certain technologies.

Top European News

- ASML Hit With New Dutch Limits on Chip Gear Exports to China

- Fevertree Drops After Bank of America Cuts to Underperform

- Polish Inflation Eases for Fourth Month, Fueling Rate Cut Bets

- ASML Says Dutch Measures Won’t Have ‘Material Impact’ on Outlook

- Germany June Adj. Unemployment Rate Rises to 5.7%; Est. 5.6%

- Swiss Chalets Become Target Amid Eastern Europe’s Property Woes

FX

- DXY remains relatively resilient and firmly underpinned, with the index forming a solid base above 103.000 between 103.23-54 parameters.

- EUR was unreactive to a batch of mixed EZ data, whilst headline inflation printed cooler than expected, although the core metrics marginally topped expectations.

- Cyclical currencies are held up fairly well on the back of buoyant risk appetite.

- Kiwi got another confidence boost from an improvement in ANZ consumer sentiment.

- Yen is flat despite more verbal intervention from Japanese officials.

- Brazil’s Finance Minister said the National Monetary Council decided to set the 2026 inflation target at 3%, while the government expects rates to fall from August, according to Reuters.

Fixed Income

- Debt futures appear destined for a bleak finish and further losses heading into month, quarter, HY-end.

- Bunds, Gilts and the T-note hover precariously over deeper intraday lows, at 133.09, 94.71 and 111-25+ respectively.

Geopolitics

- The US is expected to curb exports of some Dutch chip equipment to specific facilities in China, according to a source cited by Reuters. ASML (ASML NA) does not expect the Dutch government’s chip export measures to have a material impact on its financial outlook, according to the press release.

- Russian Foreign Minister Lavrov said he sees no argument for a Black Sea Grain Deal extension, according to a press conference.

- US State Department approved the potential sale of logistics supply support to Taiwan for an estimated cost of USD 108mln, while it approved the possible sale of 30mm ammunition and related equipment to Taiwan for an estimated USD 332mln, according to Reuters.

- Australian and EU trade ministers spoke as hopes of a free trade deal rise, according to Reuters citing sources; there is optimism a deal could be struck by mid-year. Another meeting could be held next fortnight.

Commodities

- WTI and Brent front-month futures are on a firmer footing intraday despite the firmer Dollar but as equities see cautious gains.

- Spot gold remains heavy as the Dollar extends gains, with the yellow metal threatening another breach of USD 1,900/oz to the downside this morning

- Base metals are mostly but copper bucks the trend and outperforms, with the LME 3M contract back above USD 8,250/t at the time of writing. Reports last night noted an electrical accident at Codelco’s largest copper mine – the El Teniente mine.

- HSBC lowered Brent oil price assumptions to USD 80/bl in H2’23, USD 80/bl in FY23, USD 75/b in FY24 and long-term, according to Reuters.

- Boliden’s (BOL SS) Ronnskar production partially resumed; several of production lines may have to operate at limited capacity; all other production lines at Ronnskar are expected to ready for production during July.

- Shanghai INE adjusts trading limit and margin requirements for international copper and crude oil futures, effective from settlement on July 4, according to Reuters.

US Event Calendar

- 08:30: May Personal Income, est. 0.3%, prior 0.4%

- May Personal Spending, est. 0.2%, prior 0.8%

- May Real Personal Spending, est. 0.1%, prior 0.5%

- May PCE Deflator MoM, est. 0.1%, prior 0.4%

- May PCE Deflator YoY, est. 3.8%, prior 4.4%

- May PCE Core Deflator YoY, est. 4.7%, prior 4.7%

- May PCE Core Deflator MoM, est. 0.3%, prior 0.4%

- 09:45: June MNI Chicago PMI, est. 43.8, prior 40.4

- 10:00: June U. of Mich. Sentiment, est. 63.9, prior 63.9

- June U. of Mich. Expectations, est. 61.3, prior 61.3

- June U. of Mich. Current Conditions, est. 68.0, prior 68.0

- June U. of Mich. 1 Yr Inflation, est. 3.3%, prior 3.3%

- June U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

Welcome to the last day of H1. We’ll have our full review on Monday but with a day left to go here is a quick and selected spot check of where we are in 2023 so far. The S&P 500 is +14.5%, the Nasdaq +29.9%, FANG+ +70.9%, EU Stoxx 600 +7.5%, 2 and 10yr USTs +43.4bps and -3.7bps, 2 and 10yr Gilts +170bps and +71bps, EU Crossover -68.7bps, CDX HY +1.4bps and with Crude Oil -13.47%. So in general a good half year for risk, with yield curves steepening and long-term bond yields going mostly sideways unless of course you’re in the UK. H1 has mostly been a risk rebound from stressed levels in 2022 so the performance should be put in some perspective but with AI giving things an added kicker. Let’s see what H2 brings. Much will depend on whether the US recession starts. We still think it does in Q4 with risks that it gets delayed to Q1 rather than doesn’t happen. There’s a long long way before you can be sure you’re out of the gravitational pull of the lag of aggressively tighter monetary policy over the last year or so. Remember that this time last year the ECB was only about to end QE on July 1st and hike rates at the end of that month.

The recession call was something we asked in our summer survey this week. We’ve now released the results in a slidepack (link here). It’s evident that a lot of people are pushing back their timing of the next US recession, but mostly that’s just a shift from 2023 into 2024, rather than thinking we’ll avoid one altogether. We’ve also seen more bearishness since our last survey, with a majority now expecting the next 10% move in the S&P to be down rather than up (the opposite to the last survey), whilst it’s pretty much 50/50 as to whether 10yr Treasury yields hit 4.5% or 2.5% first. For other opinions on central banks, ChatGPT and the chance of Donald Trump being President again, click on the full chartbook for more.

The big story of the last 24 hours was another strong round of US data, which triggered a massive bond selloff that sent Treasury yields to their highest levels since SVB collapsed. In particular, the latest weekly US jobless claims dropped back to 239k (vs. 265k expected), marking their biggest single-week decline since October 2021, and importantly ending a run of 5 consecutive weekly gains. Alongside that, the continuing claims fell to their lowest level since February, and the latest Q1 GDP data saw a big upward revision to a +2.0% annualised pace, having previously been estimated at +1.3%.

All this positive data played into the recent market narrative, which is that strong growth and sticky inflation will see central banks hold rates at restrictive levels for much longer than previously expected. In fact, if you look at market pricing for deep into 2024, it was clear how investors were adjusting to a much more prolonged period of high rates. For instance, expectations for the Fed’s policy rate by December 2024 moved back above 4% again to their highest level since SVB’s collapse (the low was 2.70% after peaking at 4.22% before SVB). Now admittedly, that’s still beneath the 4.6% level in the Fed’s latest dot plot, but it shows how markets are increasingly coming round to the Fed’s view of the world.

This shift was evident for the very near-term as well, with futures now pricing in a 83% chance of a July hike, the highest to date. They even see a 38% chance that by November the Fed will now deliver the second additional hike they signalled for 2023. So that’s still some way from 100%, but it goes to show how the previous scepticism towards two more Fed hikes is increasingly fading. US Core PCE will be a big event on this front today.

This re-appraisal of the outlook was very bad news for Treasuries across the board. It saw the 10yr yield surge by +13.1bps on the day to 3.84%, marking its highest level since SVB’s collapse in March. At the same time, the 2yr yield (+15.4bps) hit a post-SVB high of its own at 4.86%, and thus inverting the 2s10s curve further to -102.1bps. Meanwhile the 6m T-bill (+1.0bps) rose to its highest level since 2001, at 5.46%. It was real yields that led the gains as well, with the 2yr real yield (+12.6bps) hitting a post-2008 high of 2.79%, and another milestone was reached after the 5yr real yield crossed the 2% mark on an intraday basis for the first time since 2008 (ending the day at 1.99%).

With all eyes on central banks and the rates path, markets will now focus on today’s Euro Area flash CPI print for June, with particular attention on the core reading. Ahead of that, we got some more of the country releases yesterday, including from Germany, the largest European economy. That showed a rebound in inflation to +6.8% on the EU-harmonised measure as expected, up from +6.3% in May. In part, the rebound occurred because last year saw an offer of cheap rail tickets that dropped outside the annual comparison. But there was also an upside in Spain as well, since even as headline inflation dropped beneath the ECB’s 2% target, core inflation (on the national definition) still came in at +5.9% (vs. +5.5% expected). With the country releases so far, our Euro Area economists see slight upside risks to the +5.6% yoy headline (+5.5% core) consensus expectation for today.

We’ll have to see what today’s numbers show, but the movements in European rates very much followed what happened in the US yesterday. That included rises in yields on 10yr bunds (+10.3bps), OATs (+10.9bps) and BTPs (+12.1bps), along with a more moderate rise for gilts (+6.3bps). Similarly, investors also grew in confidence that the ECB would keep taking rates higher, and now see a 58% chance that we’ll have had two hikes by the time of the meeting-after-next in September.

Despite the rates move, equities were remarkably resilient, with the S&P 500 posting a +0.45% gain. Banks (+2.62%) led the advance amidst the prospect of higher rates, and positive US stress test results the night before, but other cyclical sectors also put in a decent performance. Indeed, the small-cap Russell 2000 advanced for a 4th consecutive day, finishing +1.23% by the close. By contrast, the NASDAQ index was unchanged (-0.00%), with the tech megacap FANG+ index underperforming (-0.75%). Back in Europe there were also modest advances, with the STOXX 600 posting a modest +0.13% gain.

Asian equity markets are mixed on the final trading day of the first half of the year. As I type, the Nikkei (-0.53%) is struggling with the Hang Seng (-0.05%) swinging between gains and losses. Otherwise, the Shanghai Composite (+0.73%), the CSI (+0.54%) and the KOSPI (+0.28%) are gaining ground this morning. In overnight trading, US stock futures are slightly higher with those on the S&P 500 (+0.07%) and NASDAQ 100 (+0.18%) printing mild gains.

Early morning data showed that China’s factory activity remained in contraction territory in June as the official manufacturing PMI came in at 49.0, barely improving from prior month’s reading of 48.8, thus adding pressure on the administration to deliver more stimulus. Additionally, the services sector also recorded its weakest reading since China abandoned its stringent COVID curbs late last year. The official non-manufacturing PMI eased to 53.2 from 54.5 in May, highlighting that the recovery in the world’s second biggest economy has lost some traction.

Elsewhere, consumer prices in Tokyo rose +3.1% y/y in June (+3.4% expected, down from the +3.2% recorded in the preceding month). Ex-food and energy came in at 3.8% vs. 4% expected. Separately, Japan’s labour market remained tight as the jobless rate remained unchanged at 2.6% in May while industrial output contracted -1.6% m/m in May, its first fall since January (v/s -1.0% decline expected) after increasing +0.7% previously.

In FX, the Japanese yen went past the 145 mark versus the US dollar in early Asia trade, touching its lowest in over seven months, prompting more intervention calls. They intervened at around 146 last year. Meanwhile, slightly hawkish comments on desired FX stability from Japan’s Finance Minister Shunichi Suzuki did trigger the pair’s retreat from 145.07 earlier to 144.71 as we go to print.

When it came to yesterday’s other data, UK mortgage approvals saw a larger-than-expected increase in May to 50.5k (vs. 49.7k expected). Furthermore, the M4 money supply came in unchanged on a year-on-year basis, which is the lowest it’s been since September 2015. Elsewhere, the European Commission’s economic sentiment indicator for the Euro Area continued to decline, with a move to a 7-month low of 95.3 in June (vs. 95.7 expected), adding to the negative trend in Euro Area data surprises over the past two months.

To the day ahead now, and data releases include the Euro Area flash CPI reading for June. In Germany, we’ll also get retail sales for May and unemployment for June. And in the US, there’s the PCE reading for May, and personal income and personal spending data.

Loading…

https://www.zerohedge.com/markets/futures-rise-apple-market-cap-tops-3-trillion

{kind=link}