- APAC stocks were mostly higher following the tech-led gains on Wall St where the Nasdaq outperformed and the S&P 500 printed a 9-month high.

- US President Biden held a call with the debt ceiling negotiation team and his team said that steady progress is being made in talks.

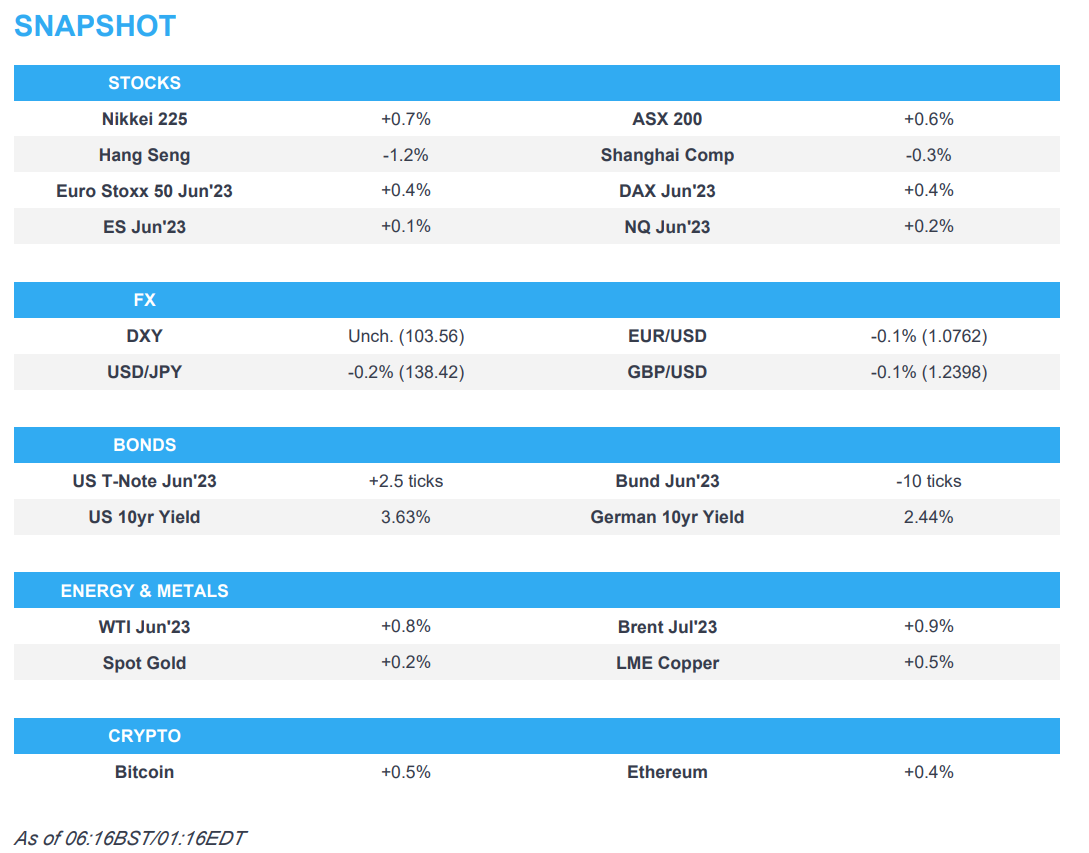

- European equity futures are indicative of a higher open with the Euro Stoxx 50 +0.4% after the cash market closed up 1.0% yesterday.

- DXY sits above the 103.50 mark following yesterday’s advances, EUR/USD and Cable languish beneath 1.08 and 1.24 respectively.

- Looking ahead, highlights include German Producer Prices, ECB Economic Bulletin, Speeches from BoE’s Haskel, ECB’s Lagarde & Schnabel, Fed’s Powell, Williams & Bowman

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were firmer with sentiment underpinned by optimism regarding a debt ceiling deal and encouraging data including a surge in the Philly Fed Manufacturing survey and a fall in initial jobless claims. All major indices were lifted and the S&P 500 tested the 4,200 level to print a 9-month high, while the Nasdaq was the outperformer amid a Big Tech bias with the heavy lifting done by the likes of Nvidia (NVDA), Amazon (AMZN), and particularly Netflix (NFLX), which saw near double-digit strength after a positive ad tier subscriber update.

- SPX +0.94% at 4,198, NDX +1.81% at 13,834, DJI +0.34% at 33,535, RUT +0.58% at 1,784.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed Discount Window loans were at USD 9.05bln in the week ended May 17th which was down from the USD 9.32bln level during the prior week, while BTFP lending was USD 87bln vs prev. USD 83.1bln W/W and the Fed’s Other Credit was at USD 208.5bln vs prev. USD 212.5bln W/W.

- Fed’s Bullard (non-voter) said higher rates are insurance against inflation and that he will keep an open mind going into the June meeting, while he reiterated the view that a fall in Treasury yields offsets banking sector tightening, according to an FT interview.

- WSJ’s Timiraos also wrote that the debt-limit impasse could soon force officials at the Fed to revisit its crisis-management playbook put together during similar fights a decade ago.

- White House officials said US President Biden held a call with the debt ceiling negotiation team and his negotiating team said that steady progress is being made in talks, while President Biden is confident that Congress will take action to avoid a US default, according to Reuters.

- US Senate Majority Leader Schumer said debt limit talks are making progress and that the Senate would act right after the House on the debt limit, while US Democratic Senator Sinema said she is beginning to feel confident that a debt agreement will occur. It was also reported that a group of Democratic Senators told US President Biden to prepare to use the 14th Amendment to avoid a debt default.

- US House GOPs in the Freedom Caucus said the Senate must pass the House GOP debt limit package and called for no more talks until the Senate takes action on the House debt limit bill, while House GOP McHenry suggested they were nowhere close to being done on debt ceiling talks.

- US House Speaker McCarthy expects the House will vote next week if an agreement is reached, according to Politico’s Everett.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following the tech-led gains on Wall St where the Nasdaq outperformed and the S&P 500 printed a 9-month high on debt ceiling optimism and firm data, although Chinese markets lagged amid disappointment from Alibaba’s revenue miss.

- ASX 200 was lifted with the tech sector front-running the gains as it took inspiration from its US counterpart and with the top-weighted financial industry trailing closely behind.

- Nikkei 225 surged at the open to print its highest since August 1990 although pared some of the gains after losing steam on its approach to the 31,000 level and as participants digested the latest CPI figures which were mostly in line with expectations but showed a faster pace of acceleration.

- Hang Seng and Shanghai Comp. were mixed with the Hong Kong benchmark pressured as tech giants suffered following Alibaba’s earnings which beat on the bottom line but missed on revenue, while frictions lingered after the US and Taiwan reached an initial agreement on a ’21st Century’ trade pact and with China concerned about recent signs of negative China-related developments at the G7.

- US equity futures plateaued after yesterday’s advances with the E-mini S&P perched above 4,200.

- European equity futures are indicative of a higher open with the Euro Stoxx 50 +0.4% after the cash market closed up 1.0% yesterday.

FX

- DXY was steady and hovered around a 2-month high firmly above the 103.00 level following the prior day’s advances due to strong US data and hawkish Fed speak which resulted in a pick-up in the pricing of odds for a June hike, while the focus now turns to Fed Chair Powell’s panel discussion later to see if he adds further to the hawkish momentum.

- EUR/USD languished at the prior day’s lows beneath 1.0800 after recent dollar strength, while there were comments from ECB’s de Guindos that there is still scope to keep raising rates but most of the tightening has already been done.

- GBP/USD failed to make any meaningful recovery and sits just below the 1.24 mark following yesterday’s selling pressure and after the recent slew of BoE commentary provided very little to shift the dial.

- USD/JPY took a breather after recent advances but with the pullback limited by the risk tone and yield differentials.

- Antipodeans were kept afloat due to their high-beta statuses and with New Zealand Trade Balance at a surplus.

- PBoC set USD/CNY mid-point at 7.0356 vs exp. 7.0392 (prev. 6.9967)

- Mexican Central Bank kept its rate unchanged at 11.25%, as expected, via a unanimous decision. Banxico stated that inflation expectations for 2023 decreased but those for the longer-term remained relatively stable at levels above target and inflation is still projected to converge to the 3% target in Q4 2024, while it considered that the economy has begun to undergo a disinflationary process given that many pressures have eased.

FIXED INCOME

- 10yr UST futures were contained after falling to their lowest levels since March in the aftermath of strong Philly Fed data, a fall in jobless claims, and hawkish comments from Fed’s Logan and Bullard.

- Bund futures remained despondent after prices trickled beneath the 134.00 level.

- 10yr JGB futures suffered amid spillover selling from global counterparts and after weaker demand at the enhanced -liquidity auction for long- to super-long JGBs.

COMMODITIES

- Crude futures gained in tandem with the constructive mood but with upside limited by recent dollar strength after hawkish Fed rhetoric and firm US data releases spurred bets for a Fed rate hike in June.

- Saudi’s Energy Minister said coordination with OPEC+ countries is a cornerstone of the efforts to enhance the stability of oil markets and maintain their balance, according to the state news agency.

- Spot gold eked mild gains with upside restricted by a steadfast dollar and lack of haven demand.

- Copper futures eventually edged higher amid the mostly positive risk environment to atone for some of yesterday’s weakness which was mainly a function of the advances in the greenback.

CRYPTO

- Bitcoin was rangebound with price action lacklustre after slipping beneath the USD 27,000 level.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi said China proposed to establish meeting and dialogue mechanisms in cooperation between China and Central Asian countries in which the mechanisms will cover agriculture, transportation, emergency management, education and political party affairs, while Xi added that China will roll out more trade facilitation measures and upgrade bilateral investment agreements with Central Asian countries.

- China’s Commerce Minister is to meet with US Commerce Secretary Raimondo and US Trade Representative Tai next week, according to Politico.

- China’s Taiwan Affairs Office said it will allow travel agencies to resume group tours for Taiwan residents to the mainland from today, according to Reuters.

- USTR office said US and Taiwan reached an initial agreement on a ’21st Century’ trade pact which covers customs and trade facilitation, good regulatory practices, services regulations, anti-corruption measures and SMEs. USTR added that further US-Taiwan negotiations will commence on additional trade areas including agriculture, digital trade, labour, environment and SOEs, according to Reuters.

DATA RECAP

- Japanese National CPI YY (Apr) 3.5% vs. Exp. 3.5% (Prev. 3.2%)

- Japanese National CPI Ex. Fresh Food YY (Apr) 3.4% vs. Exp. 3.4% (Prev. 3.1%)

- Japanese National CPI Ex. Fresh Food & Energy YY (Apr) 4.1% vs. Exp. 4.2% (Prev. 3.8%)

- New Zealand Trade Balance (Apr) 427M (Prev. -1273.0M, Rev. -1586M)

- New Zealand Exports (Apr) 6.80B (Prev. 6.51B, Rev. 6.28B)

- New Zealand Imports (Apr) 6.38B (Prev. 7.78B, Rev. 7.87B)

GEOPOLITICS

- Ukrainian President Zelensky is to travel to Japan to attend the G7 Summit in person, according to Bloomberg.

- US senior administration official said all G7 members are preparing to implement new Russian sanctions and export controls with the sanctions aimed at closing evasion loopholes and will target war inputs, energy reliance and access to financial systems. US is to target Russia with roughly 300 sanctions on individuals, entities, vessels and aircraft across Europe, the Middle East, and Asia. US sanctions will also target financial facilitators, Russia’s future energy and extraction capabilities, as well as others supporting Russia’s war, while G7 countries remain committed to upholding the price cap on Russian oil, according to Reuters.

- US President Biden’s administration signalled to European allies in recent weeks that the US would allow them to export F-16 fighter jets to Ukraine, while Ukraine was said to have used a Patriot to shoot down at least one Russian fighter jet in recent weeks, according to CNN’s Bertrand.

- US Pentagon reportedly overvalued US equipment sent to Ukraine by around USD 3bln, while the error opens up the possibility of more weapons being sent to Kyiv, according to Reuters citing sources.

- EU”s President of the European Council Michel said they will restrict the sale of Russian diamonds and call on China to pressure Russia to stop military aggression, while he said stable and constructive cooperation with China is in their interests and that they need to engage with China on global challenges.

UK/EU

- UK plans GBP 1bln of semiconductor investment in a new strategy that aims to strengthen the domestic industry and chip supply chains, according to the government.

DATA RECAP

- UK GfK Consumer Confidence (May) -27 vs. Exp. -27 (Prev. -30)

Loading…

https://www.zerohedge.com/markets/firmer-trade-following-debt-ceiling-optimism-feds-powell-ahead-newsquawk-europe-market-open

{kind=link}