With all other megatech companies reporting solid earnings, all eyes were on the results from the last giga-cap kahuna, the world’s largest company, Apple and its $3+ trillion market cap.

As previewed earlier, analysts expected Apple to report a modest revenue slowdown YoY (iPhone revenue of $49 billion, down from $50.6 billion, iPad revenue: $6.7 billion, down from $7.6 billion; Mac revenue: $7.7 billion, down from $10.4 billion; Services revenue: $21.1 billion, up from $19.8 billion and Wearables/Home/Accessories revenue: $8.5 billion, down from $8.8 billion) while EPS of 1.20 would be flat from 1.20 a year ago.

With that in mind, this is what Apple just reported for its fiscal Q2:

- EPS $1.26, up from $1.20 a year ago, and beating the estimate of $1.20

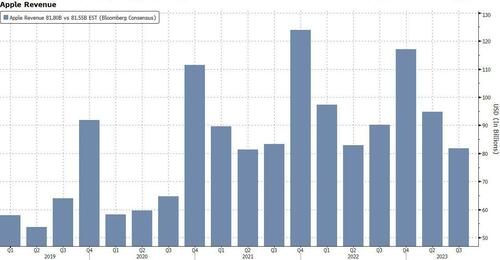

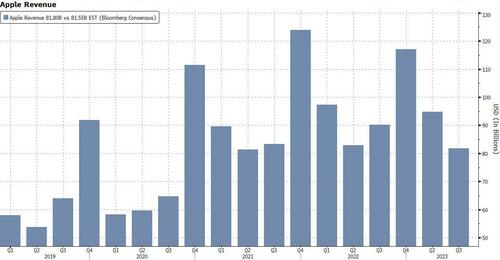

- Revenue $81.80 billion, down 1.4% y/y, but also beating estimates of $81.55 billion.

- Products revenue $60.58 billion, -4.4% y/y, missing estimates of $60.67 billion

- IPhone revenue $39.67 billion, -2.4% y/y, missing estimates of $39.8 billion

- Mac revenue $6.84 billion, -7.3% y/y, beating estimates of $6.37 billion

- IPad revenue $5.79 billion, -20% y/y, missing estimates of $6.33 billion

- Wearables, home and accessories $8.28 billion, +2.5% y/y, missing estimates of $8.38 billion

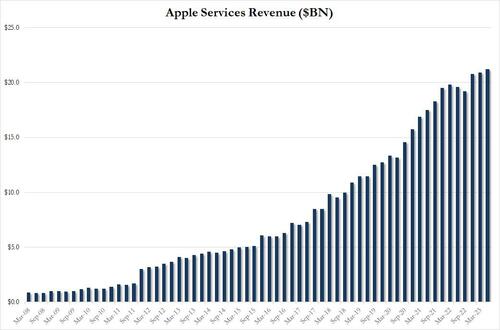

- Service revenue $21.21 billion, +8.2% y/y, beating estimates of $20.77 billion

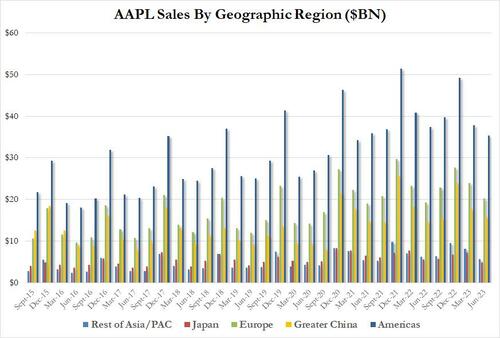

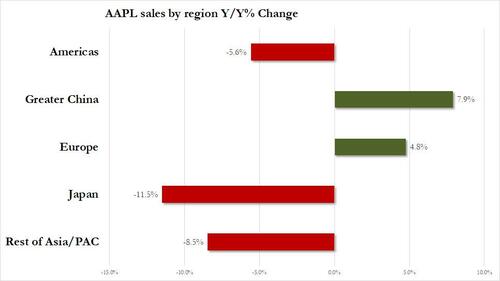

- Greater China rev. $15.76 billion, +7.9% y/y, beating estimates of $14.59 billion

- Gross margin $36.41 billion, +1.5% y/y, beating estimates of $36.03 billion

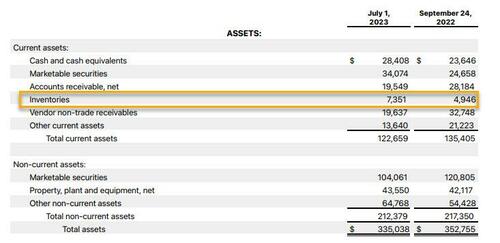

- Cash and cash equivalents $28.41 billion, +3.3% y/y, beating estimates of $24 billion

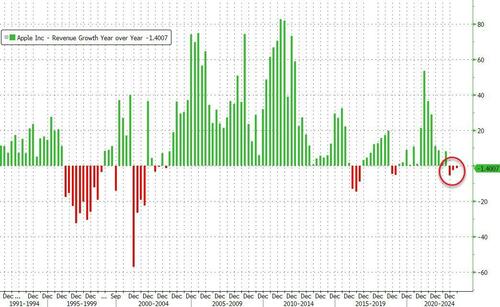

While the numbers were mixed, with revenue of almost $82 billion coming above expectations thanks to strong service revenue offsetting a miss in iPhone, iPad and wearables, what the market did not like is that this was the 3rd consecutive quarter of annual revenue declines: the first time for AAPL since 2016.

And while we wait for the company’s guidance during the 5pm call, the company did not surprise the market with another generous shareholder payout unlike last quarter when it unveiled an additional $90 billion stock repurchase (it did declare a cash dividend of 24 cents a share, payable Aug. 17). in fact, buybacks of $17.5 billion were about $1 billion below consensus and down over $2 billion vs. 2Q and could be a key area of discussion, according to Bloomberg.

Commenting on the quarter, CEO Tim Cook said that “we are happy to report that we had an all-time revenue record in Services during the June quarter, driven by over 1 billion paid subscriptions, and we saw continued strength in emerging markets thanks to robust sales of iPhone.”

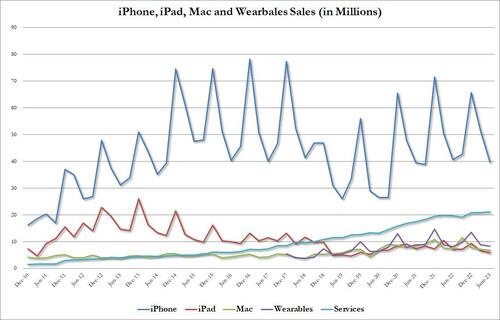

Looking at the revenue breakdown, Apple missed across almost all product categories, with the only exception a modest beat in Mac revenues:

- iPhone Revenue $39.67B, missing estimates of $39.8B (to be expected with a new model coming out next month).

- Wearables, Home & Accessories revenue of $8.28B, missing estimates of $8.38B

- Mac Revenue $6.84B, beating estimates $6.37B

- iPad Revenue $5.79B, missing estimates of $6.33B

- Total products Rev. $60.58B, missing estimates of $60.67B

As we noted last quarter, what markets may be concerned about is that AAPL appears to be reaching a “double top” in product revenue, and indeed with the exception of Services, almost every product class did slowdown from a year ago.

One place where investors may have been pleasantly surprised was China sales, which at $15.76 billion, beat estimates of $14.59 billion.

And while China’s YoY growth rate of 7.9% was impressive, this was more than offset by a slowdown in good old USA where revenues dropped by 5.6%, and while Europe rose 7.9%, Japan actually tumbled by double digits, sliding 11.5% perhaps as a result of the collapse in the yen’s purchasing power.

There was some more good news in Services revenue, which at a time when products continue to slowdown, printed at a fresh record high of $21.2 billion, a reversal to last quarter’s miss.

Putting it all together:

- The iPhone missed Wall Street expectations narrowly amid the smartphone slump and ahead of the iPhone 15.

- The iPad continues to see declines as the company releases little to no compelling new features and hasn’t changed the design of the iPad Pro since 2018.

- The Mac declined on an annual basis, but beat expectations thanks in part to the 15-inch MacBook Air and new Mac Studio.

- Wearables missed yet again as consumers await new Apple Watches.

- Services was the lone bright spot, topping $21.2 billion in the quarter and beating Wall Street expectations.

Finally, there was some more bad news, and this time not so much on the income statement but the balance sheet, where inventories unexpectedly surged from where they were at the end of September, by 49%. As Bloomberg asks, “Is that a build-up ahead of a launch or a worrying accumulation of unused components?”

Commenting on the quarter, Bloomberg Intelligence senior analyst Anurag Rana said on Bloomberg TV that he expected this be a “boring” quarter for Apple — and that “it came out this way.”

“We want to see what the next iPhone is going to do next month. … We’ve also seen supply-chain problems in China that led to the decline of shipments, and I think they need to get on a call and say they are not going to see any of that this year.”

To be sure, the market was not happy with what Apple reported – especially after it sent the company to an all time high just under $200 a few days ago, and after briefly kneejerking higher, the stock has slumped 1% after hours, dropping to one month lows, and reversing much of the post-Amazon euphoria.

Loading…

https://www.zerohedge.com/markets/apple-slides-weak-iphone-sales-inventory-surge-3rd-straight-quarter-declining-revenues

{kind=link}