In late breaking news that will shock absolutely no one, The Fed reports that the 23 largest US banks passed their annual stress tests.

Including Credit Suisse…

“Today’s results confirm that the banking system remains strong and resilient,” Vice Chair for Supervision Michael S. Barr said.

“At the same time, this stress test is only one way to measure that strength. We should remain humble about how risks can arise and continue our work to ensure that banks are resilient to a range of economic scenarios, market shocks, and other stresses.”

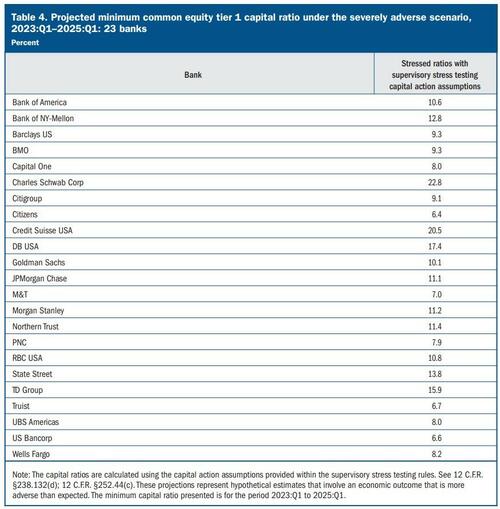

The aggregate and individual bank post-stress common equity tier 1 (CET1) capital ratios remain well above the required minimum levels throughout the projection horizon.

The regulator’s yearly stress testing of the banks, which it started performing after the 2008 financial crisis, revealed that they could withstand a 40% drop in commercial real estate prices and aggregated losses of more than half a trillion dollars without failing.

The scenarios that the 23 biggest banks faced also included a severe economic recession, 10% unemployment and a large drop in home prices.

For the first time, the Board conducted an exploratory market shock on the trading books of the largest banks, testing them against greater inflationary pressures and rising interest rates. This exploratory market shock will not contribute to banks’ capital requirements but was used to further understand the risks with their trading activities and to assess the potential for testing banks against multiple scenarios in the future. The results showed that the largest banks’ trading books were resilient to the rising rate environment tested.

The $541 billion in total projected losses includes over $100 billion in losses from commercial real estate and residential mortgages, and $120 billion in credit card losses, both higher than the losses projected in last year’s test. The aggregate 2.3 percentage point decline in capital is slightly less than the 2.7 percentage point decline from last year’s test but is comparable to declines projected from the stress test in recent years.

The results vary significantly across the institutions based on banks’ business lines, portfolio composition, and securities and loan risk characteristics, which drive changes in the magnitude and timing of loss, revenue, and expense projections.

So now we just wait for the next bank to blow up? And remember – no one could have seen that coming.

Read the full stress test report here:

Loading…

https://www.zerohedge.com/markets/surprise-fed-says-all-big-banks-passed-stress-tests

{kind=link}