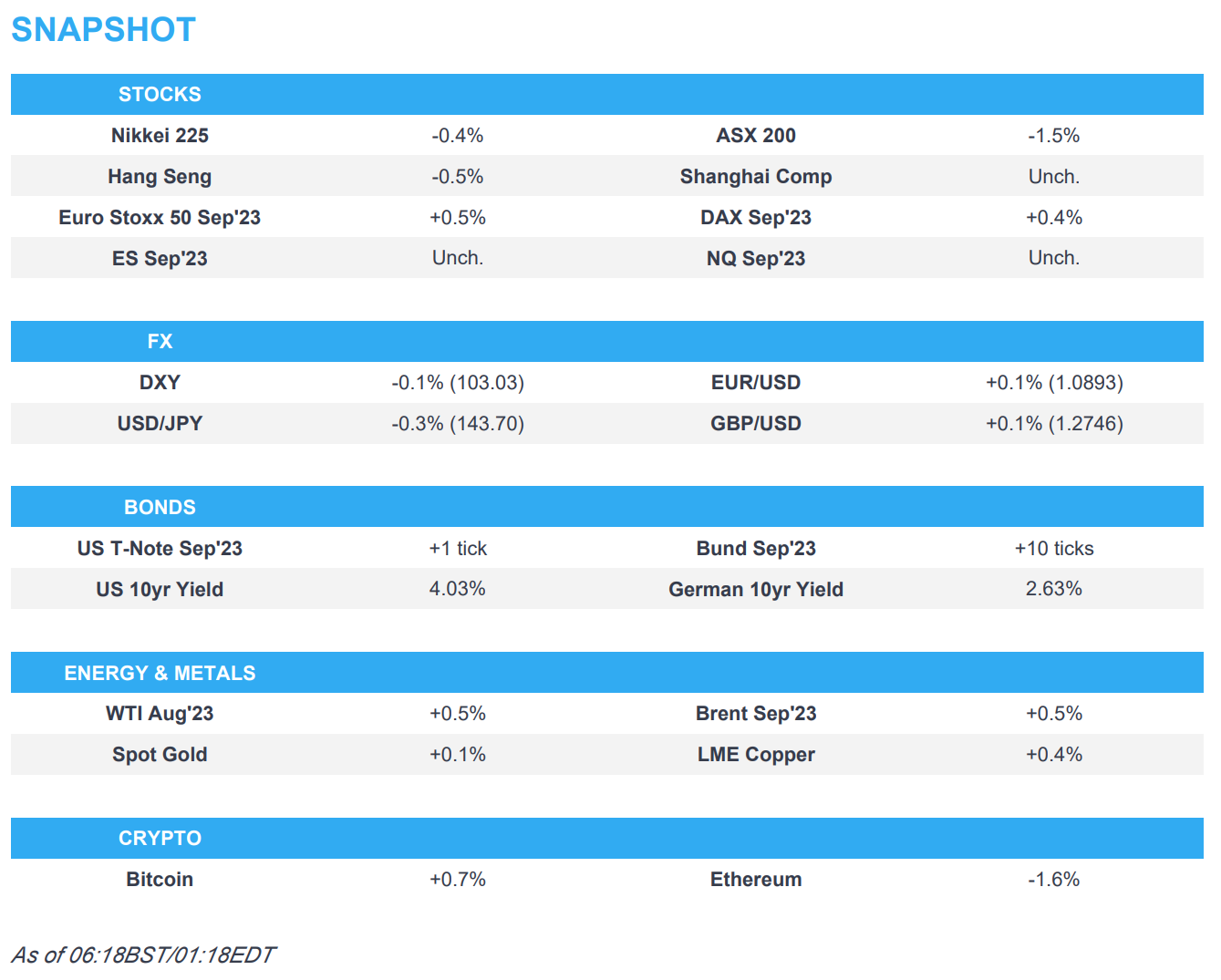

- APAC stocks were mostly lower amid spillover selling from global peers including in the US where the major indices were pressured.

- DXY remained confined to within a narrow range as price action calmed down from yesterday’s fluctuations, USD/JPY traded on both sides of the 144.00 level.

- European equity futures are indicative of a slightly higher open after the Euro Stoxx 50 cash closed down by 2.9% yesterday.

- Some key purchasers of Saudi Arabia’s crude in Asia and Europe are seeking lower volumes for next month after the kingdom hiked official prices and extended output cuts, according to Bloomberg.

- Looking ahead, highlights include German Industrial Production, US NFP Report, Canadian Jobs Report Speeches from ECB’s Lagarde & de Guindos.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were pressured, and bonds were also hit as participants digested several firm data releases including hot ADP employment, sub-250k jobless claims and a spike in ISM Services which further spurred hawkish Fed pricing and resulted in particular weakness in the cyclical/value areas.

- SPX -0.79% at 4,412, NDX -0.75% at 15,089, DJI -1.07% at 33,923, RUT -1.64% at 1,842.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed Discount Window borrowing was at USD 3.4bln on July 5th (prev. 3.2bln on June 28th), ‘Other Credit’ was at USD 164.8bln (prev. 168.3bln W/W) and BTFP lending was at USD 103bln (prev. 103.1bln W/W).

APAC TRADE

EQUITIES

- APAC stocks were mostly lower amid spillover selling from global peers including in the US.

- ASX 200 suffered its largest intraday drop since March with real estate and tech front running the declines across all sectors as Australian bond yields climbed.

- Nikkei 225 slumped at the open following disappointing Household Spending data which showed a surprise monthly contraction although the index bounced off its lows and recouped around half of the earlier losses.

- KOSPI was dragged lower by weakness in index-heavyweight Samsung Electronics after its preliminary Q2 earnings in which operating profit topped forecasts but slumped by 96% Y/Y.

- Hang Seng and Shanghai Comp conformed to the downbeat mood as growth concerns and trade frictions lingered and with little hope of any breakthrough during US Treasury Secretary Yellen’s trip to China.

- US equity futures flatlined amid the risk-off mood across Asia and ahead of the key US jobs data.

- European equity futures are indicative of a slightly higher open with the Euro Stoxx 50 +0.4% after the cash market closed down by 2.9% yesterday.

FX

- DXY remained confined to within a narrow range as price action calmed down from yesterday’s fluctuations and as participants braced for the incoming Non-Farm Payroll report.

- EUR/USD was lacklustre following the recent failure to reclaim the 1.0900 status.

- GBP/USD traded flat amid a lack of drivers and after the prior day’s swings through the 1.2700 focal point.

- USD/JPY traded on both sides of the 144.00 level with Japan’s currency largely ignoring the latest data releases.

- Antipodeans marginally gained but with upside capped amid the lack of data releases and as the broad risk aversion mostly offset the rise in yields across the Tasman.

- PBoC set USD/CNY mid-point at 7.2054 vs exp. 7.2423 (prev. 7.2098)

FIXED INCOME

- 10yr UST futures were rangebound as participants await the NFP report.

- Bund futures languished near multi-month lows but are off worst levels after a floor held around 131.00.

- 10yr JGB futures tracked the losses in global peers amid the absence of additional purchases by the BoJ and after mixed data releases from Japan including firmer-than-expected labour cash earnings.

COMMODITIES

- Crude futures eked marginal gains following the prior day’s whipsawing and inventory-fuelled rebound.

- Some key purchasers of Saudi Arabia’s crude in Asia and Europe are seeking lower volumes for next month after the kingdom hiked official prices and extended output cuts, according to Bloomberg.

- Spot gold was flat alongside an uneventful dollar as participants await the incoming US jobs data.

- Copper futures traded sideways as the recent strong data releases from the US are counterbalanced by expectations of higher interest rates.

CRYPTO

- Bitcoin gained overnight and climbed back above the USD 30,000 level despite the risk aversion.

NOTABLE ASIA-PAC HEADLINES

- China’s Finance Ministry said it hopes the US will take concrete actions to create a favourable environment for the healthy development of economic and trade ties between China and the US, according to Reuters.

- China Customs banned the imports of food from 10 prefectures in Japan and noted the IAEA report on Japan releasing water from the Fukushima plant did not fully reflect the views of all experts involved in the assessment process, while it added that the Japanese side still has many problems in the legitimacy of sea discharge.

- BoJ Deputy Governor Uchida said they will maintain YCC from the perspective of sustaining easy monetary conditions and that the risk of missing the chance to hit 2% inflation with premature policy is bigger than being too late in tightening monetary policy, while he added there is a huge distance to ending negative rates, according to Nikkei.

DATA RECAP

- Japanese All Household Spending MM (May) -1.1% vs. Exp. 0.5% (Prev. -1.3%)

- Japanese All Household Spending YY (May) -4.0% vs. Exp. -2.4% (Prev. -4.4%)

- Japanese Overall Labour Cash Earnings (May) 2.5% vs. Exp. 0.7% (Prev. 1.0%, Rev. 0.8%)

GEOPOLITICS

- Ukrainian military spy chief said the threat is receding at the Zaporizhzhia nuclear plant, according to Reuters.

- Japanese Economic Minister Goto said they are aware that New Zealand received Ukraine’s request to join the CPTPP, while he added that they must carefully assess whether Ukraine fully meets the high level of CPTPP agreement in terms of market access and rules, according to Reuters.

- US Navy said Iran’s Revolutionary Guards seized a commercial ship in the Gulf’s international waters which was possibly engaged in smuggling activity, while the US Navy deployed maritime assets to monitor but did not respond to the event.

EU/UK

NOTABLE HEADLINES

- UK reportedly plans to reverse the MiFID II ban on free research for clients, according to Bloomberg.

- UK trade union RMT said rail workers will take a week of strike action on the London Underground from July 23rd in a dispute over pensions and working conditions.

- ECB’s Nagel said rates will have to remain high for a longer period and he does not see the threat of excessive tightening currently but cannot say yet where interest rates will peak.

Loading…

https://www.zerohedge.com/markets/softer-equity-trade-action-more-contained-elsewhere-pre-nfp-newsquawk-europe-market-open

{kind=link}