US equity futures climbed rose for a fifth consecutive session – the longest winning streak since August – ahead of the September CPI report that’s expected to show further slowing in US inflation, which should cement the market’s conviction that the Fed’s hiking cycle is over. As of 8:00am, S&P 500 futures are up 0.4% and above Wednesday’s highs, following almost 1% gain for Estoxx 50, Nasdaq futures rose 0.3%. Treasuries were flat trading at 4.55%, while the dollar is slightly weaker ahead of key US consumer prices data. WTI crude futures are higher by 0.8%, paring Wednesday’s drop as commodities catch a bid with all 3 segments higher.

The latest FOMC minutes point to a paused Fed (according to JPM, confirmation is expected to come from Powell coming on Oct 19) with the debate now on how long to maintain at this level before cutting; Fedspeak puts R-star in the 2.5% – 3% range. China invites US SecDef to its Defense Forum; biggest olive branch of the year? Asian stocks gained after China’s state fund looks to increase its stake in the country’s biggest banks; will look to do more over next six months.

In premarket trading, Ford slipped in pre-market trading after union members went on strike at its largest plant, a highly profitable pickup factory in Kentucky. First Solar advanced after Barclays upgraded the stock to overweight. Birkenstock gained 0.7% after dropping from its initial public offering on Wednesday. Here are some other notable premarket movers:

- Beyond Meat fell 5.5% after Mizuho Securities cut the recommendation to underperform from neutral, pointing to macroeconomic pressures for consumption and a “lack of disruptive innovation” in the area.

- Carvana (CVNA) drops 2% after long-term bull BNP Paribas Exane cut its rating on the online platform for buying used cars to neutral from outperform.

- E2open (ETWO) drops 4.1% after being downgraded to neutral from buy at Redburn Atlantic, which said it “underestimated the hurdles” faced by the software company transitions from M&A-driven to organic growth.

- First Solar Inc. (FSLR) shares are up 3.6% after Barclays upgraded the company to overweight from equal-weight.

- PepGen (PEPG) jumps 13% after the company said the FDA has lifted a full clinical hold and cleared its application, allowing PegGen to initiate an early-stage study of its treatment for patients with myotonic dystrophy, a genetic disorder.

- Target Corp. (TGT) climbs 2.1% following an upgrade to buy from neutral at BofA, which sees an improved risk profile for the retailer based on recent pullback in the stock.

- Tempest Therapeutics (TPST) is slumping a day after the stock closed up nearly 4,000%. Shares of the drug developer are down 38% ahead of the open.

The market’s attention turns next to Thursday’s US consumer price data (full preview here) which economists are forecasting to show a further easing in inflation. CPI is forecast to have slowed to an annual rate of 3.6% in September from 3.7% the previous month, according to a Bloomberg survey. Data published Wednesday showed prices paid to producers rose by more than forecast in September, bolstered by higher energy costs.

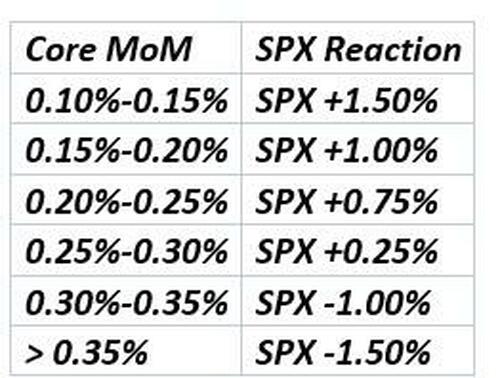

In its preview of the CPI print, Goldman writes that “Stocks have squeezed 4 trading sessions and counting since the guts of the NFP data last Friday were deemed goldilocks .. The tape remains resilient in the midst of the tragic geopolitical developments .. I think this rally continues today if CPI is 30bps (or softer).”

Here is Goldman’s market reaction matrix:

Meanwhile Fed officials are taking a more patient approach now that rates are at or near their peak, Boston Fed President Susan Collins said Wednesday. Her Atlanta counterpart Raphael Bostic said the central bank doesn’t need to keep tightening unless inflation’s descent starts to stall.

“The less hawkish turn that we’ve seen from the Fed is in part to try and reduce the volatility that we’ve seen in rates markets and to try and bring expectations down to a more reasonable level,” Mehvish Ayub, senior investment strategist at State Street Global Advisors, said on Bloomberg Television.

European stocks are on track to rise for a third consecutive session The Stoxx 600 is up 0.7% to a three-week high. Energy shares led gains as oil rebounded after OPEC+ leaders Saudi Arabia and Russia reaffirmed their close cooperation to support the crude market. Mining and media stocks also outperformed while banks lagged, with Barclays Plc falling as much as 3.8% after Chief Executive C.S. Venkatakrishnan said stagnant deal activity, easing volatility and peaking interest rates are set to weigh on the sector’s earnings. Among individual movers, Publicis Groupe climbed as much as 5.1% to the highest level since April after the advertising agency upgraded its full-year organic growth target on the back of stronger-than-expected 3Q sales growth. Growth in the Epsilon unit — Publicis’s data management business — and a smaller tech industry exposure than peers helped the company outrun the broader slowdown in ad spending, analysts say. EasyJet Plc fell after the airline said it will order an additional 157 Airbus SE A320neo jets, with an option to add 100 more. Here are the most notable European movers:

- Stabilus shares rise as much as 9.2% after agreeing to acquire Destaco from Dover for $680 million. The deal is seen improving profitability for the maker of gas springs and motion-control products, according to the analysts.

- Suedzucker shares gain as much as 6.4%, the most since July, after the market leader in European sugar reported forecast-beating results, which Warburg attributes to strong profitability in the sugar segment.

- Outokumpu shares gain as much as 5.9%, the most since May, after Bloomberg reported the Finnish steelmaker will supply some of the stainless steel panels for the exterior of Tesla’s new Cybertruck pickup truck. The Helsinki-based company is Europe’s largest stainless-steel manufacturer.

- Restaurant Group shares rise as much as 38% and trade slightly above the level of a recommended cash offer from private equity group Apollo that values the owner of Wagamama at £506 million ($623 million). At least two analysts see the offer price as too low.

- Ericsson shares fluctuate, rising as much as 2.2% as the telecom equipment maker booked a charge for 50% of the goodwill and other intangible assets attributed to Vonage, which the Swedish company acquired in 2022. Analysts say the writedown is largely expected and could be a clearing event, although it may reinforce investors’ views that the deal was a poor use of capital.

- Helvetia shares drop as much as 4.7%, and is weakest stock on Thursday in the Stoxx 600 insurance index, after Berenberg cuts to sell and says underwriting margins are deteriorating with new accounting changes “covering the cracks.”

- Darktrace shares fall as much as 7.4% after the British AI company issued a trading update for 1Q24. Analysts drew attention to softer-than-expected annual recurring revenue figures, though also noted Darktrace’s positive growth versus other UK companies.

- Oxford Instruments shares fall as much as 7.1%, the most since June 2022, after the UK laboratory technology firm forecast full-year performance toward the lower end of expectations.

- EasyJet shares drop as much as 4.8% after the low-cost airline in its trading update posted what Morgan Stanley calls “slightly soft” revenue per seat in the fourth-quarter, with Citi highlighting a miss in pricing. The carrier also placed its biggest-ever aircraft order.

- Dowlais shares fall as much as 2.8% after JPMorgan downgraded its rating to neutral from overweight. The broker says it’s turning cautious on growth drivers at the automotive technology company and is waiting for more clarity on business prospects in electric vehicles.

- Bossard shares drop as much as 1.1% after the Swiss industrials company forecast full-year sales below the average analyst estimate. Analysts noted declining end-market demand for the maker of fastening devices and industrial adhesives, while currency headwinds also played a part.

Earlier in the session, Asian stocks were headed for a sixth straight day of gains, as a move by China’s sovereign wealth fund to buy bank shares lifted sentiment, while investors parsed the less hawkish commentary by the Federal Reserve. The MSCI Asia Pacific Index rose as much as 1.1% on Thursday, led by consumer discretionary and industrial shares. Equities in Japan and South Korea were among the best performers in the region.

- Chinese stocks listed in Hong Kong jumped more than 2% after China’s state-owned Central Huijin Investment Ltd. increased its stake in the nation’s biggest banks for the first time since 2015, a sign that authorities may double down on efforts to support the struggling stock market.

- Japan’s Nikkei 225 was boosted on a break above the 32,000 level following softer-than-expected PPI data and comments from BoJ Board Member Noguchi who continued to toe the dovish line.

- Australia’s ASX 200 was led higher by early outperformance in its top-weighted financial industry although the gains in the index were limited as energy and the defensive sectors lagged.

- Key stock gauges in India were little changed after Tata Consultancy Services’ warning of weakening US tech spending led to a rout in IT stocks. The S&P BSE Sensex was steady at 66,408.39 in Mumbai, while the NSE Nifty 50 Index also ended almost flat, bucking the regional trend as most peers extended gains. A gauge tracking IT stocks in India fell 1.5%, the most in two weeks.

In FX, the Bloomberg Dollar Spot Index is down 0.1% having earlier touched its lowest in almost two weeks; it is set for the longest run of losses in over three years after more Federal Reserve officials suggested that US interest rates may have peaked. The Swiss franc and Swedish krona are the best performers among the G-10’s; the kiwi is the laggard. The pound dipped, snapping a six-day rising streak, after figures showed the UK economy registered a modest rebound in August as the dominant services sector offset another weak month for manufacturers and construction firms.

The dollar has corrected lower as dovish Fedspeak drives a rebound in Treasuries, “but its too early to conclude this is the start of a USD downtrend,” said Carol Kong, a strategist at Commonwealth Bank of Australia in Sydney, adding that the US CPI reading “could again change the narrative and push the USD back up”

In rates, treasuries were little changed, as investors await a reading of US CPI later in the day to better gauge the outlook for inflation and rates. Yields are unchnaged on the day in front-end and belly of curve and marginally cheaper at long-end. All are within about 1bp of Wednesday’s closing levels with price action limited ahead of key inflation data. US 10-year yield little changed around 4.56% while bunds and gilts trail by 1bp and 1.5bp in the sector. Slight underperformance of long end moves 5s30s spread from daily low near 10bp to ~13bp, while 2s10s spread is minimally flatter on the day. Core European rates are slightly cheaper across the curve in early London session: gilts and bunds decline, with UK and German 10-year yields both gaining 2bps. Treasury auction cycle concludes with 30-year reopening at 1pm, follows 10-year auction Wednesday which tailed by 1.8bp. Fed Reserve Bank of Dallas President Lori Logan, Fed Bank of Atlanta President Raphael Bostic and Fed Bank of Boston President Susan Collins are due to speak later in the day.

In commodities, oil prices rose, with WTI gaining 1% to trade near $84.30. Spot gold adds 0.4%. Bitcoin was lacklustre following a recent retreat to beneath the USD 27,000 level.

To the day ahead now, and data releases include the US CPI release for September, the weekly initial jobless claims, and UK GDP for August. From central banks, we’ll hear from the Fed’s Logan, Bostic and Collins, the ECB’s Elderson, Villeroy, Holzmann, Knot, Vujcic, Vasle and Panetta, along with the BoE’s Pill. The ECB will also release the account of their September meeting.

Market Snapshot

- S&P 500 futures up 0.3% to 4,421.50

- MXAP up 1.2% to 159.79

- MXAPJ up 0.9% to 500.53

- Nikkei up 1.7% to 32,494.66

- Topix up 1.5% to 2,342.49

- Hang Seng Index up 1.9% to 18,238.21

- Shanghai Composite up 0.9% to 3,107.90

- Sensex little changed at 66,433.04

- Australia S&P/ASX 200 little changed at 7,090.98

- Kospi up 1.2% to 2,479.82

- STOXX Europe 600 up 0.6% to 455.82

- German 10Y yield little changed at 2.73%

- Euro little changed at $1.0625

- Brent Futures up 0.9% to $86.61/bbl

- Gold spot up 0.3% to $1,880.86

- U.S. Dollar Index down 0.14% to 105.67

Top Overnight News

- Shares advanced before a report that’s expected to show a slowing in US inflation, which will help shape the outlook for the Federal Reserve’s next steps. A move by China’s sovereign wealth fund to buy shares of the country’s largest banks fueled further optimism.

- US Secretary of State Antony Blinken landed in Tel Aviv Thursday on a hastily arranged diplomatic trip. Israeli jets hit key targets in Gaza after the nation vowed to wipe out Hamas, which is designated a terrorist group by the US and European Union.

- A monthly report on US consumer prices due Thursday is set to muddy the picture for Federal Reserve officials trying to decide whether to hike interest rates again, especially as escalating conflict in the Middle East adds uncertainty, according to Bloomberg Economics.

- Bond investors are starting to back away from what’s been one of the few bright spots for them this year amid signs yields may have peaked after the epic rout in September.

- The yen’s weakness is so entrenched that even ending the Bank of Japan’s negative-rates policy may fail to save it.

- China has told its securities firms and their offshore units to stop conducting illicit cross-border business, including brokering shares and selling funds to domestic investors, in a bid to plug regulatory loopholes.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were firmer after the region took impetus from the intraday rebound on Wall St where dovish Fed rhetoric offset the hot PPI data, while stale FOMC Minutes provided no major fireworks. ASX 200 was led higher by early outperformance in its top-weighted financial industry although the gains in the index were limited as energy and the defensive sectors lagged. Nikkei 225 was boosted on a break above the 32,000 level following softer-than-expected PPI data and comments from BoJ Board Member Noguchi who continued to toe the dovish line. Hang Seng and Shanghai Comp. were underpinned in which the Hong Kong benchmark gapped above the 18,000 level and spearheaded the advances in the region, while Chinese banks were buoyed after China’s sovereign wealth fund raised its stake in the largest banks for the first time since 2015.

Top Asian News

- Chinese securities regulator banned brokerages and their offshore units from taking on new mainland clients for offshore trading and it set an end-October deadline for the removal of apps and websites soliciting mainland clients, according to Reuters sources.

- China studies easing foreign stake limits in Chinese firms, via Bloomberg. In-fitting with reports seen in late September. Total overseas ownership in local firms is currently capped at 30%

- Chinese GDP growth might slow in Q3 to above 4.0% Y/Y from 6.3% growth in Q2 but is expected to improve after Q3, according to Securities Daily.

- BoJ Board Member Noguchi said the biggest focus is whether wage hike momentum will be maintained or not and the raising of the YCC band does not signify a tightening of monetary policy, while he added when inflation expectations are rising, some flexibility is needed to continue easy policy under YCC. Furthermore, Noguchi said there are signs upward price pressures are coming down and the BoJ’s near-term mission is to realise a situation where wage growth does not fall short of inflation as soon as possible through persistent monetary easing.

European bourses are trading with modest gains in the wake of the late gains on Wall Street yesterday and the upbeat APAC session overnight. Sectors in Europe are mostly firmer with Basic Resources and Energy top of the leaderboard, whilst Banks lag to the downside. US futures are trading on the front foot, continuing the strength seen in yesterday’s session, with the hotter-than-expected PPI print unable to cap sentiment in the run-up to today’s CPI.

Top European News

- BoE’s Dhingra said they think only about 20%-25% of the impact of interest rate hikes has been fed through to the economy and suggested that when growth is as slow as it is now, the chances of a recession or not recession are going to be pretty equally balanced so they should be prepared for that and it is not going to be great times ahead. Furthermore, she added that if growth falls by much more than the BoE expects from here, a cut may happen sooner, according to the BBC.

- BoE’s Pill said finely balanced issue if the BoE still has more to do. A lot of policy tightening is yet to come through. Inflation in the UK remains too high, according to Reuters. Pill said it is premature from policy perspective to be discussing unwinding policy; we may become overly sensitive to short-term fluctuations in data.

- ECB’s Stournaras sees no value in bringing forward the end of PEPP and sees no reason to raise banks’ requirements. He added that Italy’s government must reassure the European Commission and investors, according to Reuters.

- ECB’s Makhlouf said the ECB will have a better feel on rates after December. He added Italian bond spread will focus the ECB.

- ECB’s Wunsch said monetary policy is at the right level. Inflation shock from increasing oil prices could lead to an additional rate hike. When asked about whether October will see a PEPP announcement, said PEPP should be discussed, according to Reuters.

- ECB’s Villeroy said monetary patience is currently more important than activism; duration is more important than level, according to Reuters.

FX

- Dollar is depressed ahead of US CPI data after brief bounces post-PPI and FOMC minutes – DXY edges closer to chart prop within tight 105.530-730 confines.

- Franc remains firm on safe-haven grounds – USD/CHF probes 0.9000 and EUR/CHF nearer 0.9550 than 0.9600.

- Euro retains 1.0600+ status vs Buck and is surrounded by hefty option expiry interest.

- Yen is still drawn to 149.00 against Greenback as BoJ’s Noguchi sticks to dovish guidance.

- Cable unstable above 1.2300 amidst mixed UK macro releases and BoE members highlighting the extent of hikes in the pipeline.

Fixed Income

- Debt futures fade after another strong rally to fresh cycle peaks for Bunds and Gilts.

- 10-year German and UK benchmarks towards a base of 129.59-130.20 and 94.83-95.66 respective ranges.

- T-note also consolidating pre-US CPI, IJC and latest Fed speak within narrow 108-09/00+ confines.

- Italy sells EUR 6.5bln vs exp. Italy to sell EUR 5.25-6.5bln 3.85% 2026, 4.00% 2030, 4.45% 2043 BTP & EUR 1.5bln vs. Exp. EUR 1-1.5bln 4.00% 2035 BTP Green.

Commodities

- Crude front-month futures have been grinding higher throughout the European morning despite any fresh macro catalysts and as investors look ahead to US CPI.

- Dutch TTF prices are once again on the grind higher after pulling back yesterday, with the complex still underpinned by Chevron’s Australian LNG situation alongside the suspected sabotage of the Baltic-connector gas pipeline in the run-up to winter heating season.

- Spot gold continues grinding higher despite the recovery of the Dollar as geopolitical premium continues to be baked into the yellow metal.

- US Private Inventory Report (bbls): Crude +12.9mln (exp. +0.5mln), Cushing -0.5mln, Gasoline +3.6mln (exp. -0.8mln), Distillates -3.5mln (exp. -0.8mln).

- IEA OMR: raises 2023 oil demand forecast to 2.3mln BPD (vs. prev. 2.2mln BPD), cuts 2024 to 880k BPD (vs. prev. 1mln BPD) amid weaker economic environment and efficiency improvements. The pullback in oil reflects demand destruction. Israel-Hamas conflict has not had a direct impact on oil flows; ready to act to keep the market well-supplied if needed. OPEC+ voluntary cuts will keep the market in deficit in Q4 but could shift to a surplus if extra cuts are unwound in January. Russian total oil exports rose 460k BPD in September.

- Saudi Energy Minister said the oil market should not be left alone; we should be proactive given numerous challenges.

- Russian Deputy PM Novak said the market is very sensitive but the balance; we quickly react to the situation in the oil market where there are many uncertainties; global economy is growing slower than expected. He added global oil demand will increase by 2.4mln BPD this year. He added that Russia lowered exports of oil and oil products, and Russian OPEC+ commitments include oil product exports.

- Iraq oil ministry spokesperson said OPEC+ priorities include achieving stability and balance in global markets. Severity of impact from security events on supply/demand flows depends on how long such events last. OPEC+ does not deal with fast reactions to challenges that face the market. Iraq is committed to voluntary cuts, according to Reuters.

- Grain storage facility and grain was damaged in Russian drone attack on Ukraine’s Odesa region, according to Reuters.

Geopolitics

- Russia and India are in talks about a summit this year between President Putin and PM Modi, according to Ria.

- Iran’s Foreign Minister is to travel to Lebanon amid the Israel-Palestine events, according to Tasnim citing the ambassador.

- US Secretary of State Blinken has landed in Israel, according to Reuters witness.

- US President Biden said the US is sending military assistance to Israel and they made it clear to the Iranians to “be careful”. Furthermore, President Biden held a call with UAE’s President and stressed his condemnation of Hamas, while the leaders discussed the importance of ensuring humanitarian assistance reaches those in need.

- US believes that Iran knew about the Hamas attack plan but not the timing and scale of the attack, according to WSJ.

- China Commerce Ministry on reports of the EU planning an anti-subsidy probe of Chinese steelmakers said EU’s action is against international trade offer, according to Reuters.

- A Committee of Russia’s Parliament lower house has drafted legislation to revoke the treaty on the nuclear test ban, according to Ria.

US Event Calendar

- 08:30: Oct. Initial Jobless Claims, est. 210,000, prior 207,000

- Sept. Continuing Claims, est. 1.68m, prior 1.66m

- 08:30: Sept. CPI MoM, est. 0.3%, prior 0.6%

- Sept. CPI YoY, est. 3.6%, prior 3.7%

- Sept. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

- Sept. CPI Ex Food and Energy YoY, est. 4.1%, prior 4.3%

- 14:00: Sept. Monthly Budget Statement, est. -$146b, prior -$429.8b

Central Bank Speakers

- 10:00: Fed’s Logan Delivers Welcoming Remarks

- 13:00: Fed’s Bostic Delivers Welcoming Remarks

- 16:00: Fed’s Collins Speaks at Banking Conference

DB’s Jim Reid concludes the overnight wrap

I’ll be spending most of today telling my wife “you really, really don’t look your age.. but how does it feel to be married to a younger man from a different half-century”. Yes, she turns 50 today. I have exactly 8 months before the same fate awaits me so I won’t be able to make too much fun of her. In terms of festivities, she’s off to a spa day today and then we’re out to dinner tonight as a family. Then tomorrow night we’ve booked a ridiculously expensive hotel in London for our first night away together from the kids since we’ve had them, with theatre and dinner thrown in. Then on Sunday she’s seeing Madonna live at the o2 arena as she starts her world tour (Madonna not my wife). I’ll be ducking out at that point and will be en route to New York for work. Next year we’re having a joint 100th party at home which will be the hottest ticket in town (I live in a very small town).

The hottest ticket in town today will be ring side seats to the latest US CPI report. Our economists are looking for headline CPI at +0.26%, which will slightly outpace core, which they see at +0.24%. This would put the YoY at 3.5% and 4.0%, respectively, down 0.2pp and 0.4pp from last month. See their preview here along with a link to register for their webinar afterwards.

Ahead of this important print, markets this week have responded more to central bank speak than the tragic events in the Middle East, but the two combined have provided the perfect conditions for bonds to rally. With oil softening again yesterday (WTI down -2.88%), it’s now only around one percent higher than before the weekend attacks on Israel.

10yr US bonds go into the big release some -31.5bps beneath their intraday peak last Friday immediately after the jobs report, with yesterday seeing a further -9.5bps move lower. We saw a sharp London morning rally on the back of Bloomberg headlines of missiles being fired from Lebanon towards Israel. Much of this rally then reversed, in part after a 10yr auction that saw softer demand from indirect bidders, but bonds rallied again later on after the release of the Fed September minutes. The big story was a significant flattening in the Treasury curve, with the 2yr yield up +1.3bps to 4.98%, whilst the 30yr yield came down -13.8bps to 4.69%, its largest daily decline since March at the height of the banking turmoil. Overall, there was lots of talk about steepeners being a crowded trade and helping to create the fairly sudden flattening of late. We have a 30yr auction today to test this recent long-end outperformance.

This out-performance got added support from Fed commentary. First, there were remarks from Fed Governor Waller, who said that that financial markets were “tightening up and they are going to do some of the work for us”. Then in the US afternoon we had the minutes from the Fed’s September meeting. These repeated some key messages from last month’s press conference, with all FOMC members agreeing that “policy should remain restrictive for some time” and that the Fed “can proceed carefully”. But there were also some dovish hints as “risks to the achievement of the committee’s goals had become more two-sided”. The minutes added focus to the details of today’s CPI print, noting that “significant progress in reducing inflation had yet to become apparent in the prices of core services excluding housing”.

The Fed commentary saw investors further discount the likelihood of a hike at the next meeting in November, with futures only giving it a 10% likelihood now, down from 14% the previous day and 31% last Friday after the strong payrolls. Those moves to price out further tightening came in spite of a strong US PPI inflation print for September yesterday. The monthly gain in headline PPI was at +0.5% (vs. +0.3% expected), whilst PPI excluding food and energy was up +0.3% (vs. +0.2% expected). In turn, that pushed the year-on-year measure for headline PPI up to +2.2%, which is a clear recovery from its low of +0.2% back in June.

Even with the latest fall in long-term borrowing costs, yesterday brought fresh evidence that the recent sharp increase was still filtering through. That came from the Mortgage Bankers Association, whose latest data showed the 30yr fixed mortgage rate was up to 7.67% in the week ending October 6, which is the highest it has been since 2000 .

Over in Europe, there was also a significant flattening in the yield curve, with yields on 10yr bunds (-5.7bps), OATs (-6.2bps) and BTPs (-6.2bps) all moving lower, even as the 2yr yields all rose. That came amidst several speakers from the ECB yesterday, including Dutch central bank governor Knot, who said that returning inflation to target in 2025 “would be an acceptable return for me”. Bundesbank President Nagel also said in a CNBC interview that “pausing could be an option” .

For equities, yesterday saw a moderate advance on both sides of the Atlantic, with gains for the S&P 500 (+0.43%) and Europe’s STOXX 600 (+0.15%). The S&P 500 had traded a few tenths lower in the middle part of the session but rallied in the last couple of hours, assisted by a renewed decline in yields. Tech stocks led the moves in the US, with the NASDAQ (+0.71%) and the FANG+ Index (+0.99%) seeing stronger advances, whilst energy stocks in the S&P 500 (-1.35%) underperformed amidst the decline in oil prices. Over in Europe there was a divergence by country, with Germany’s DAX (+0.24%) and Italy’s FTSE MIB (+0.36%) posting gains but France’s CAC 40 fell -0.44% as luxury giant LVMH fell -6.46% after reporting disappointing Q3 sales growth .

Turning back to oil prices, WTI crude was down -2.88% to $83.49/bl yesterday, and this morning it’s down a further -0.48% to $83.09/bbl. In addition to the fading of imminent concerns over supply risks from the Middle East, the reversal was helped by the latest monthly EIA report. This projects that US oil output will reach an all-time high of 13.16m barrels a day in Q4-23. Sticking to the topic, our commodities analyst Michael Hsueh updated his oil price projections in an oil market update yesterday.

Overnight in Asia, we’ve seen that broadly positive performance continue in markets, with gains for all the major equity indices. The Hang Seng (+1.89%) is leading the way, and was supported by the news that China’s sovereign wealth fund, had bought shares in some of the nation’s biggest banks. That said, the equity advances were spread across the region, with gains for the Nikkei (+1.66%0, the CSI 300 (+0.97%), the KOSPI (+0.94%) and the Shanghai Comp (+0.82%). US and European equity futures are also pointing higher, with those on the S&P 500 up +0.27% after 4 consecutive advances for the index already .

In US political news, late yesterday we heard that Rep. Steve Scalise was selected as the nominee for Speaker by a ballot of Republicans in the House of Representatives, defeating Trump-backed Rep. Jim Jordan. Scalise still faces a challenge to be elected Speaker as he can afford to lose support of at most four House Republicans to get the 217 votes needed. If Scalise is confirmed as Speaker, investors will be keen to see whether he can facilitate a spending deal ahead of the next government shutdown deadline on November 17th. In other news out of the US overnight, the UAW auto union’s strike expanded to Ford’s largest pickup plant in Kentucky. This arguably marks the largest escalation since the UAW strikes began in mid-September.

There wasn’t much other data yesterday, but we did get the ECB’s Consumer Expectations Survey for August. That showed expectations at the 1yr horizon up a tenth to 3.5%, and they were also up a tenth at the 3yr horizon to 2.5%. Overnight, however, Japan’s PPI inflation for September fell more than expected to +2.0% year-on-year (vs. +2.4% expected), which is its slowest pace in two-and-a-half years .

To the day ahead now, and data releases include the US CPI release for September, the weekly initial jobless claims, and UK GDP for August. From central banks, we’ll hear from the Fed’s Logan, Bostic and Collins, the ECB’s Elderson, Villeroy, Holzmann, Knot, Vujcic, Vasle and Panetta, along with the BoE’s Pill. The ECB will also release the account of their September meeting.

Loading…

https://www.zerohedge.com/markets/futures-rise-5th-straight-session-ahead-closely-watched-cpi-print

{kind=link}