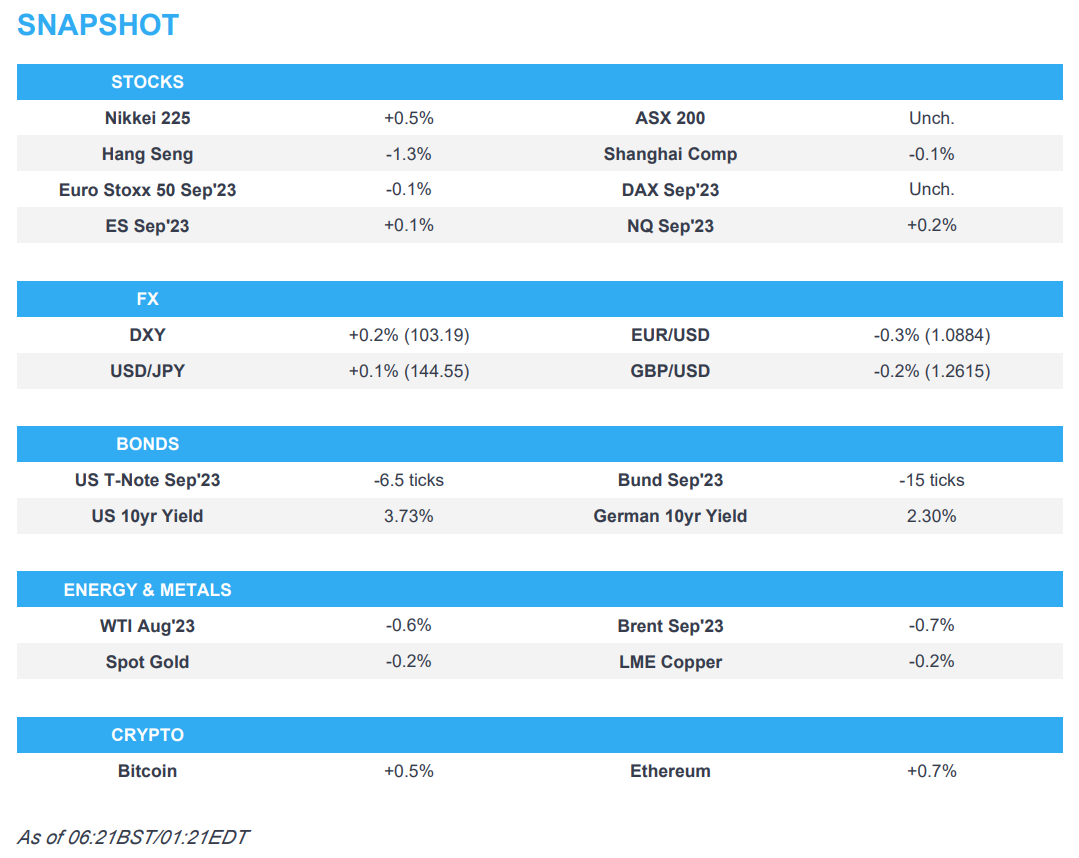

- APAC stocks traded mixed amid some indecision heading closer towards month/quarter/half-year end and after the choppy performance stateside.

- US bank shares were marginally supported after-hours following the Fed’s stress test results which all 23 of the largest banks passed.

- European equity futures are indicative of a flat open with the Euro Stoxx 50 +0.4% after the cash market closed up 0.9% yesterday.

- DXY is back on a 103 handle, EUR/USD slipped below 1.09, USD/JPY retained a footing above 144.50.

- Looking ahead, highlights include German CPI, Spain CPI, US PCE Prices (Final), IJC & GDP (Final), Riksbank Policy Announcement, remarks from Fed’s Powell & Bostic, BoE’s Tenreyro & ECB’s de Cos.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks finished mixed after a choppy performance with catalysts for risk sentiment on the light side and as participants digested the slew of central bank commentary from the Sintra Forum which continued to point to further rate hikes. Nonetheless, the SPX finished flat and the NDX notched modest gains after shaking off the negative Nvidia-related sentiment throughout the session.

- SPX -0.04% at 4,377, NDX +0.12% at 14,965, DJIA -0.22% at 33,853, RUT +0.47% at 1,859.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed said 23 banks tested showed projected losses of USD 541bln in stress tests but maintain capital ratios well above required levels, while the stress tests showed large banks are well positioned to continue lending in a severe recession and their trading books were resilient to a rising rate environment.

- US Treasury Secretary Yellen said the Treasury is monitoring the commercial real estate sector very closely and expects some losses to banks from changes in commercial real estate. Yellen said the US will address supply chain risks in areas such as EV, minerals and solar panels, while she also commented that inflation is now about 5% but remains too high.

- US CBO forecasts US public debt at 181% of GDP in 2053 vs 98% in 2023, while it projects a slightly lower long-term debt-to-GDP ratio than in February 2023 and July 2022 due to spending caps in the debt ceiling bill.

APAC TRADE

EQUITIES

- APAC stocks traded mixed amid some indecision heading closer towards month/quarter/ half-year end and after the choppy performance stateside as global markets digested the slew of central bank rhetoric from the Sintra Forum.

- ASX 200 was kept afloat as strength in the tech and telecom sectors offset the losses in utilities, real estate and miners, with some encouragement also from better-than-expected Australian Retail Sales.

- Nikkei 225 extended on gains and briefly climbed back above 33,500 as it coat-tailed on the recent advances in USD/JPY and after Japanese Retail Sales topped forecasts.

- Hang Seng and Shanghai Comp were subdued amid ongoing frictions and the potential for additional US tech export restrictions on China but with losses in the mainland cushioned by the PBoC’s liquidity efforts.

- US equity futures were rangebound with only slight gains seen as bank shares were supported after-hours following the Fed’s stress test results which all 23 of the largest banks passed.

- European equity futures are indicative of a flat open with the Euro Stoxx 50 +0.4% after the cash market closed up 0.9% yesterday.

FX

- DXY extended its gains and reclaimed the 103.00 status.

- EUR/USD was softer and breached support at the 1.0900 level to the downside despite the slew of commentary from ECB officials who kept the door wide open for a September hike.

- GBP/USD remained lacklustre after recently giving up the 1.2700 status and failed to benefit from the comments by BoE Governor Bailey and a forecast from Goldman Sachs for another 50bps rate hike in August.

- USD/JPY retained a firm footing above the 144.00 level after the prior day’s ascent to YTD highs.

- Antipodeans attempted to nurse recent losses with only brief support seen from the PBoC’s firmer-than-expected CNY reference rate setting and after Australian Retail Sales topped forecasts.

- PBoC set USD/CNY mid-point at 7.2208 vs exp. 7.2540 (prev. 7.2101)

- SNB’s Maechler said underlying price dynamics are persistent and inflation pressures are too high to create trust in money, while she added that inflation is becoming more broad-based in Switzerland.

FIXED INCOME

- 10yr UST futures reversed some of the prior day’s advances which had been led by the belly amid a strong 7yr auction and month-end anticipation.

- Bund futures held on to most of their recent gains after having shrugged off the slew of hawkish central bank commentary from Sintra, while the focus now turns to the incoming inflation data from German states.

- 10yr JGB futures were kept afloat but with gains only mild despite a firmer 2yr JGB auction.

COMMODITIES

- Crude futures lacked excitement and marginally pulled back after yesterday’s inventory-driven surge.

- Norway’s Industri Energi Labour union has agreed to a wage deal for oil drilling workers and will not go on strike, while agreements were also made with DSO and SAFE labour unions.

- Spot gold was stuck near yesterday’s lows as the greenback continued to strengthen.

- Copper futures were subdued amid ongoing US-China frictions and central bank rate hike expectations.

CRYPTO

- Bitcoin was rangebound with price action choppy but remained above the USD 30,000 level.

- Binance’s current EUR fiat deposit partner Paysafe will no longer provide services to the exchange after September 25th, according to CoinDesk.

- US President Biden wants to close tax loopholes for crypto traders and hedge fund managers.

NOTABLE ASIA-PAC HEADLINES

- US Treasury Secretary Yellen said the US will continue to take actions to protect national security interests with regards to China even if that imposes some economic cost, while she hopes to travel to China and wants to re-establish contact, as well as discuss disagreements, according to an interview with MSNBC.

- Top US diplomat for East Asia Kritenbrink said they have seen a clear and upward trend of Chinese coercion in the South China Sea and China’s provocative behaviour poses risks for businesses, while Kritenbrink also said the US and China discussed ways to increase commercial flights in a phased manner.

- Chinese Embassy Spokesman Liu Pengyu said US and China working groups will discuss the journalist issue and said China has not seen positive US initiatives on semiconductors, while Liu added that the US must remove sanctions before military talks with China.

- Chinese balloon that flew over the US earlier this year reportedly used American-made equipment to spy on Americans, while preliminary US findings showed the craft collected photos and videos but didn’t appear to transmit them, according to WSJ.

- US officials reportedly consider tightening the export of AI chips to China based on computing power in which an update to the rules may come by late July, according to Reuters sources, although one source cautioned that such US actions involving China often get delayed.

- Nvidia (NVDA) CFO said they are aware of reports on new China export restrictions but expect no material change to earnings from rules, while the CFO added that China accounts for 20%-25% of Data Centre sales and the China export ban will result in a loss of opportunities.

DATA RECAP

- Japanese Retail Sales MM (May) 1.3% vs Exp. 0.8% (Prev. -1.1%)

- Japanese Retail Sales YY (May) 5.7% vs. Exp. 5.4% (Prev. 5.0%)

- Australian Retail Sales MM (May) 0.7% vs. Exp. 0.1% (Prev. 0.0%)

- New Zealand ANZ Business Confidence (Jun) -18.0% (Prev. -31.1%)

- New Zealand ANZ Activity Outlook (Jun) 2.7% (Prev. -4.5%)

GEOPOLITICS

- EU is preparing to offer ‘security commitments’ to Ukraine although some member states are reportedly wary of the French-led plan to offer Kyiv assurances, while it was also reported that Denmark said the EU should not lower the bar to take in Ukraine, according to FT.

- US State Department approved the potential sale of integrated air and missile defence battle command system and related equipment to Poland for an estimated USD 15bln.

- European Diplomats told Iran they plan to retain ballistic missile sanctions due to expire in October, according to Reuters citing sources.

- Israeli PM Netanyahu said he wants to find a middle ground on court-system changes in Israel and regarding Ukraine, while he added Israel couldn’t allow the US to give Ukraine the Iron Dome air-defence system developed jointly with the US and he has conveyed his concerns to Russia about growing military ties with Iran, according to WSJ.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Hunt and the CMA agreed to bring forward the update of competition and unit pricing in the grocery sector to earlier in July, while the UK Treasury said the BoE will finalise their plan of action on the food supply chain and margins with further details set out in August.

- ECB’s Centeno said “we are reaching the time when monetary policy may pause and that we are very close”, according to Reuters.

- ECB’s Stournaras said a July hike is likely if the baseline develops as they think, while he added it is too early to say what the ECB will do in September and he cannot say if July will be the last hike.

- ECB’s Villeroy said inflation expectations remain well anchored and he is more confident about a soft landing but not without pain.

- ECB insiders are reportedly reasonably relaxed about the current pace of QT and suggest the passive run-off of the balance sheet could be sufficient for now, according to Econostream.

Loading…

https://www.zerohedge.com/markets/asian-stocks-traded-mixed-heading-quarter-end-and-global-markets-digested-slew-central-bank

{kind=link}