After last week’s shocking fudge by The Fed – which turned $28.4 billion of deposit outflows (NSA) into $102.5 billion of deposit inflows – we are anxiously awaiting tonight’s H8 data to see what shenanigans Powell and his pals have in store for us now.

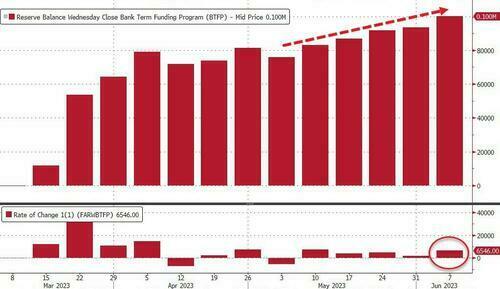

Bear in mind, before the data is unveiled, that yesterday saw yet another surge in money-market fund inflows (to a new record high) and another surge in the usage of The Fed’s emergency bank funding facility (topping $100 billion for the first time).

Source: Bloomberg

And of course, regional bank stocks were up for the 4th straight week as they ignore the ongoing real (NSA) deposit outflows that continue.

After last week’s huge seasonally-adjusted inflows, total US Commercial Bank deposits rose for the 3rd straight week, by $46.6 billion during the week ended 5/31…

Source: Bloomberg

Which seems a little odd given the massive MM fund inflows – that’s quite a decoupling?

Source: Bloomberg

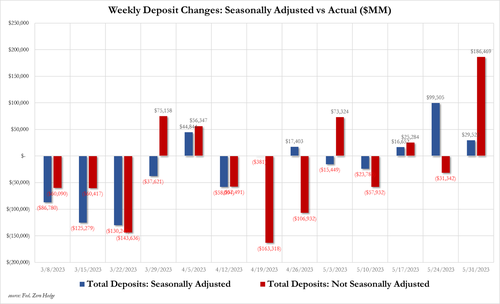

The data gets even funkier as total deposits exploded by a stunning $191.5 billion non-seasonally-adjusted – that’s the biggest weekly inflow since March 2021…

Source: Bloomberg

To put that in context, here is SA vs NSA domestic bank deposits flows… and we are still supposed to trust these guys?

A $186.5 billion NSA deposit inflow vs $31.5 billion NSA outflow last week and a $29.5 billion SA inflow this week…

On the other side of the ledger, loan volumes rose only very modestly…

Source: Bloomberg

So despite massive inflows, banks are only extending loans very sparingly… just as former Dallas Fed head Robert Kaplan explained recently:

Phase one was an asset/liability mismatch at several banks

Phase two began with the stock market deciding to do its own supervisory scrubbing

We are now heading into the third phase.

Bank leadership at small and midsize banks are considering how to shrink their loan books in order to address the mark-to-market loss of capital, as well as to guard against potential deposit instability in the future.

Bank leadership is very aware that the economy is slowing, and that we are likely about to enter a challenging credit environment.

While asset/liability mismatches are relatively easy to spot, assessing the quality of loan portfolios is much more complicated.

CEOs of many small and midsize banks are in a tough position.

They can’t easily raise equity because their stock prices are down.

As a result, they are turning to shrinking their loan books, finding places to pull back on existing loans and future loan commitments.

This is making it much harder for small and midsize businesses to get and keep their bank loans.

It is a quiet phase that won’t make headlines but is nevertheless relentlessly going on beneath the surface.

Read the full interview here…

Free to speak his mind, Kaplan concludes rather ominously, “the recent banking turmoil has highlighted the disparity between too-big-to-fail banks and smaller and midsize banks. I worry that increasing the Fed funds rate from here may create further strains on the deposit base for those smaller banks. I’m concerned that, as the Fed raises rates, it is tightening the vice on small and midsize banks and the small and midsize businesses that rely on those banks for funding.”

For now it appears The Fed has resorted to “baffle ’em with bullshit” tactics on the deposit data.

Loading…

https://www.zerohedge.com/markets/fed-fkery-continues-massive-non-seasonal-bank-deposit-inflow

{kind=link}