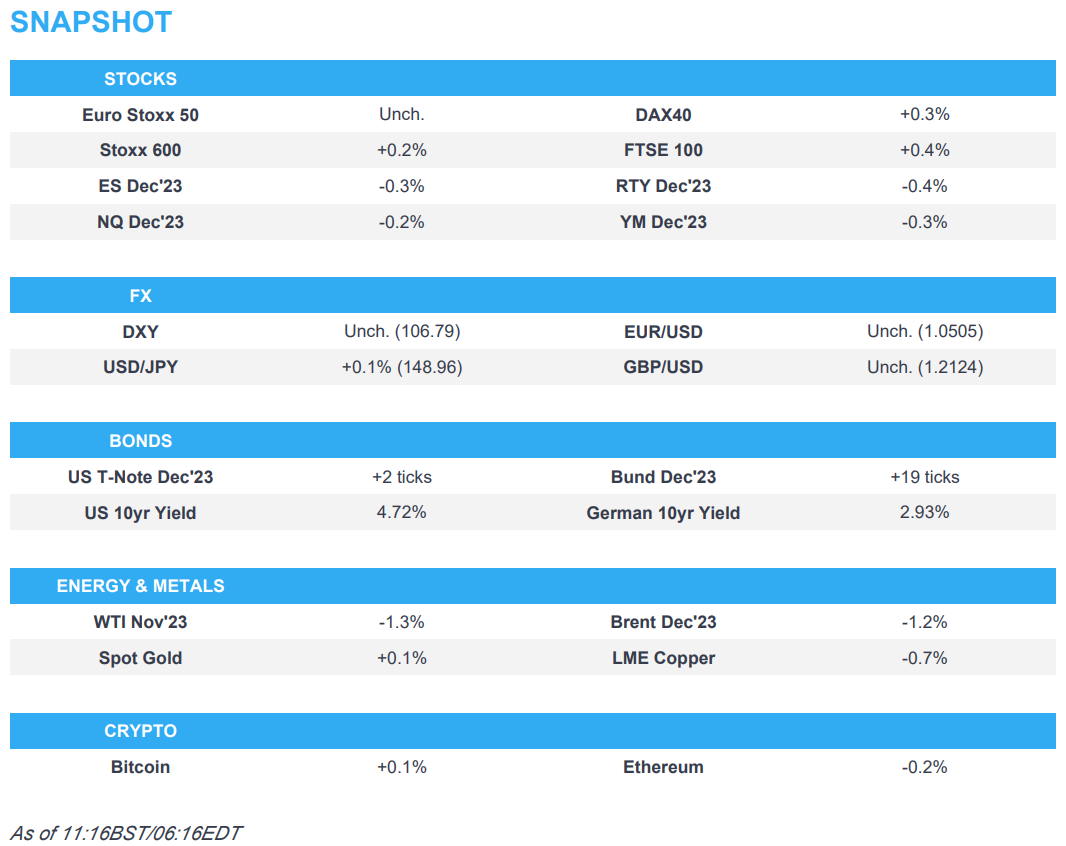

- European bourses are choppy but ultimately trade flat at the time of writing in what has thus far been a session void of incremental macro news.

- DXY index remains relatively contained between 106.500-840 confines; Antipodeans narrowly outperform; Pound was flagging even before a more contractionary than feared UK construction PMI.

- Having bounced further Wednesday’s lows, bonds are showing traits of fatigue and a reversion to the bear trend that was in place before their midweek reprieve.

- Crude futures remain on the backfoot following yesterday’s mammoth decline which saw both contracts settle lower by over USD 5/bbl apiece.

- Looking ahead, highlights include US IJCs & Challenger Layoffs, Fed’s Mester, Barkin, Daly, Barr, ECB’s Nagel, de Guindos, and Villeroy.

5th October 2023

- Click here for the Newsquawk Week Ahead summary.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are choppy but ultimately trade flat at the time of writing in what has thus far been a session void of incremental macro news.

- Sectors in Europe are mixed, with outperformance in the Travel & Leisure sector as airlines welcome yesterday’s pullback in crude prices. Conversely, to the downside, Energy names lag.

- US futures saw broad-based losses with sentiment turning sour since the European cash open, coinciding with a slight rise in yields.

- Click here for more details.

FX

- DXY index remains relatively contained between 106.500-840 confines and the Buck stayed broadly softer awaiting Challenger Layoffs, jobless claims and NFP on Friday for the next major fundamental driver.

- Antipodeans narrowly outperform with the AUD gleaning support from a wider-than-expected trade surplus.

- Pound was flagging even before a more contractionary than feared UK construction PMI. Cable remains capped by the 10 DMA and retreated towards 1.2100.

- Fix demand and exporter supply underpinned the Yen on the way from sub-149.00 to 148.27, and before the upturn in yields.

- Click here for more details.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Having bounced further Wednesday’s lows, bonds are showing traits of fatigue and a reversion to the bear trend that was in place before their midweek reprieve.

- Bunds have regrouped after their retreat to 127.21 and are back above par alongside Eurozone peers bar Bonos.

- Gilts are underwater following a reverse from 92.37 to 91.94, irrespective of a deeper than anticipated contraction in the UK construction PMI.

- T-notes are lagging within a 107-09/106-31+ range ahead of Challenger Layoffs, jobless claims, trade and another busy slate of Fed orators.

- France sold EUR 9.94bln vs exp. EUR 9-10.5bln 3.50% 2033, 2.50% 2043, and 3.00% 2054 OAT.

- Spain sold EUR 6.44bln vs exp. EUR 5.5-6.5bln 3.50% 2029, 2.35% 2033 and 1.00% 2042 Bono.

- Click here for more details.

COMMODITIES

- Crude futures remain on the backfoot following yesterday’s mammoth decline which saw both contracts settle lower by over USD 5/bbl apiece.

- Dutch TTF is softer despite a twist in the Australian LNG saga in which unions are likely to vote to resume strikes at Chevron facilities after Australia’s Offshore Alliance said Chevron reneged on commitment given to FWC

- Spot gold is flat intraday awaiting tomorrow’s US labour market report, with the yellow metal uneventful within yesterday’s USD 1,815.50-30.39/oz parameters.

- Australian Union Representative said members are likely to vote to resume strikes at Chevron (CVX) facilities in meetings commencing later tonight, according to Reuters. Australia’s Offshore Alliance said Chevron reneged on the commitment given to FWC to incorporate recommendations into Co’s EBA’s for Wheatstone and Gorgon facilities; members called a meeting at 19:00 tonight for all members on a day shift or off-facility.

- Turkish Energy Minister said the Iraq-Turkey pipeline is operational as of Wednesday and no obstacle to shipping oil to global markets; when asked about oil flows started on the pipeline, and added that Turkey stands ready to ship incoming oil, via NTV.

- Russia’s President Putin ordered to consider the introduction of regulated fuel oil prices during the heating season, via Tass.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- ECB’s Kazimir said September EZ core inflation confirmed ECB expectations and reiterated that he believes the last rate hike was the final one. He said we need to be convinced we are at the top of the rate cycle based on data available in December and March meetings, and when asked what would trigger a December hike, said this is not a scenario I’d like. He added we are trajectory of declining inflation, and inflation decline is taking somewhat longer. Kazimir added we should not at the moment use other tools such as balance sheet until we are certain we do not need to hike rates further, according to Reuters.

- ECB’s de Guindos said the current level of interest rates to help tame inflation; adding “we’re data dependent”. He added it is premature to discuss rate cuts.

- Low water levels after recent dry weather are preventing cargo vessels from sailing fully loaded on the Rhine river in Germany, with surcharges added to usual freight rates, according to traders cited by Reuters.

- BoE Monthly Decision Maker Panel data – September 2023: One-year ahead CPI inflation expectations increased slightly to 4.9% in September, up from 4.8% in August. Three-year ahead CPI inflation expectations remained flat at 3.2% in September. Expected year-ahead wage growth remained unchanged at 5.1% on a three-month moving average basis, though the single month reading for September at 5.2% was 0.2 percentage points higher than in August.

DATA RECAP

- EU HCOB Construction PMI (Sep) 43.6 (Prev. 43.4)

- German HCOB Construction PMI (Sep) 39.3 (Prev. 41.5)

- French HCOB Construction PMI (Sep) 43.7 (Prev. 42.4)

- Italian HCOB Construction PMI (Sep) 49.8 (Prev. 47.7)

- UK S&P Global/CIPS Construction PMI (Sep) 45.0 vs. Exp. 49.9 (Prev. 50.8)

- German Trade Balance, EUR, SA* (Aug 2023) 16.6B vs. Exp. 15.0B (Prev. 15.9B, Rev. 17.7B)

- German Imports MM SA* (Aug 2023) -0.4% vs. Exp. 0.5% (Prev. 1.4%, Rev. -1.3%)

- German Exports MM SA* (Aug 2023) -1.2% vs. Exp. -0.4% (Prev. -0.9%, Rev. -1.9%)

NOTABLE US HEADLINES

- UK’s Ofcom on UK cloud market said it referred the UK cloud market to CMA for investigation; says particularly concerned about the position of market leaders Amazon (AMZN) and Microsoft (MSFT), as reported by Reuters sources on Tuesday.

- Alphabet’s Google (GOOG) users have been given “better control over their data” by the German Cartel Office, according to Reuters.

- Ford (F) is to lay off an additional 400 workers due to strikes with the total layoffs tied to strikes now at 1,330 employees.

- Click here for the US Early Morning Note.

CRYPTO

- Bitcoin is modestly subdued but remains north of USD 27,500 with price action uneventful.

APAC TRADE

- APAC stocks traded higher as risk assets found reprieve after yields eased back from recent peaks following weak US ADP jobs data and a slump in oil prices.

- ASX 200 was positive following mostly improved trade data and with the gains led by yield-sensitive sectors including real estate and tech.

- Nikkei 225 outperformed on bargain buying with the index set to snap a five-day losing streak.

- KOSPI gained as participants shrugged off the firmer-than-expected CPI data which the BoK expects to stabilise into year-end.

- Hang Seng initially lagged amid very light news flow and the continued absence of mainland participants, while the latest Hong Kong PMI data printed at a deeper-than-previous contraction. However, the momentum eventually picked up in Hong Kong amid the brightened mood across regional counterparts and after Sunac China’s offshore debt restructuring plans received court approval.

NOTABLE ASIA-PAC HEADLINES

- Alibaba’s (9988 HK) logistics arm in Liege, Belgium is under scrutiny from Belgian intelligence over the use of sensitive data, according to FT.

- Sunac China’s (1918 HK) offshore debt restructuring plans received approval from a Hong Kong court.

- US Commerce Secretary Raimondo said TikTok poses national security risks, while she hopes to make some chips funding announcements this fall, according to Reuters.

- Taiwan is to probe four firms accused of helping Huawei build chip plants although Taipei said no violations of US trade sanctions have been confirmed so far, according to Nikkei.

- Apple (AAPL) supplier Foxconn (2317 TW) says Q4 is expected to grow significantly compared to Q3; with H2 a traditional peak season for the ICT industry, operations will ramp up sequentially. New product launch in September led to a strong revenue growth compared to prev. quarter, but the revenue experienced a decline YoY due to a high base. In Q3 for cloud and networking products, due to conservative customers pull-in revenue experienced a decline YY. For September, due to increasing allocations in smart consumer electronics products and rising shipment in auto components, revenue for components and other products showed significant growth YY, according to Reuters.

DATA RECAP

- South Korean CPI MM (Sep) 0.6% vs. Exp. 0.3% (Prev. 1.0%)

- South Korean CPI YY (Sep) 3.7% vs. Exp. 3.4% (Prev. 3.4%)

- Australian Trade Balance (AUD)(Aug) 9.6B vs. Exp. 8.7B (Prev. 8.0B)

- Australian Exports MM (Aug) 4.0% (Prev. -2.0%)

- Australian Imports MM (Aug) 0.0% (Prev. 3.0%)

Loading…

https://www.zerohedge.com/markets/equities-choppy-dxy-lacklustre-antipodeans-outperform-bonds-bounce-us-ijc-due-newsquawk-us

{kind=link}